process-of-preparing-income-statement-from-trial-balance

-This question was submitted by a user and answered by a volunteer of our choice.

In the Income Statement, the Trading account represents the first part and the Profit & Loss account represents the second part.

The trading account gives the overall purview of all trading activities, such as the purchase and sale of products. It is prepared to ascertain gross profit or gross loss. The profit & Loss account gives the final working results of the business. It is prepared to ascertain net profit or a net loss.

Steps to prepare Income Statement from Trial Balance

All the debit side items related to expenses and credit side items related to income listed in the trial balance shall be posted on the debit side and credit side of the income statement respectively.

1. Post opening stock on the debit side of the income statement.

2. Post purchases and sales on the debit and credit side respectively. Deduct purchase return from Purchases and sales return from Sales to arrive at the Net Purchases and Net Sales.

3. Post all the direct expenses incurred for the purchase & production of goods eg. wages, factory rent, custom duty, carriage inward, manufacturing expenses, etc on the debit side.

4. Post the amount of closing stock stated in the adjustments.

5. Make all the necessary adjustments, if any, related to outstanding and prepaid expenses, goods withdrawn for personal use, goods destroyed, etc

6. Now, find out the gross profit or gross loss.

If the total of credit side > total of debit side ie. credit balance, then the amount of difference is gross profit.

If the total of debit side > total of credit side ie. debit balance, then the amount of difference is gross loss.

7. Carry forward the ascertained gross profit to the credit side or gross loss to the debit side of the second part of the income statement ie. profit & loss account.

8. Post all the indirect expenses such as office or administrative expenses, financial expenses, selling or distribution expenses, etc on the debit side of the income statement.

9. Post all the indirect incomes such as commission received, rent received, dividend received, etc on the credit side of the income statement.

10. Consider all the necessary adjustments, if any, such as outstanding and prepaid expenses, outstanding and pre-received income, reserve for doubtful debts.

11. Calculate depreciation and amortization on the assets and post the amount on the debit side.

12. Now, find out the net profit or net loss.

If the total of credit side > total of debit side ie. credit balance, then the amount of difference is net profit.

If the total of debit side > total of credit side ie. debit balance, then the amount of difference is a net loss.

These steps complete the process of preparation of income statement from trial balance.

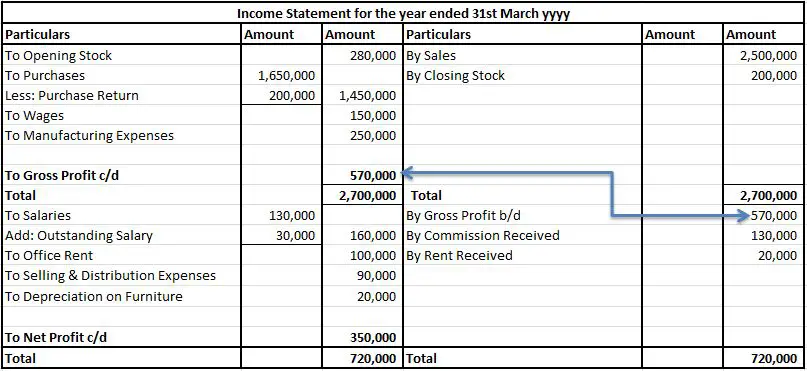

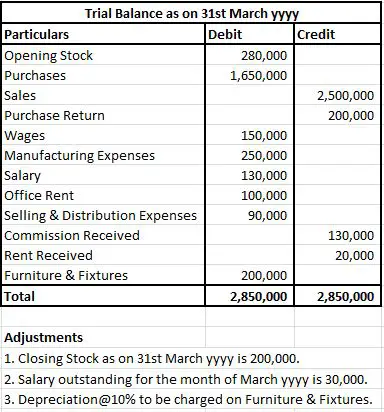

Illustration

A snippet of the trial balance and income statement has been attached for better understanding.

Prepare Income Statement from the above-given Trial Balance.