Overview of Fees Earned

Fees earned signify the revenue generated by an entity that is engaged in rendering services to its clients. When an entity deals in both goods and services it charges fees for the part of services rendered and for the goods delivered it charges the predetermined price. It generally forms a major part of revenue in the service industry such as professions where consultancy fees are charged to its clients.

Few Instances wherein an entity record the amount earned as fees:

1. For Services Rendered

- Consultancy

- Consultancy on Taxation-Related Matters

- Auditing and Assurance

- Architectural Services

- Accountancy and Other Legal Services.

2. Both Goods and Services

- Manufacturing and repairs

- Trading in goods and consultancy

- Goods and transport

When a combined amount is received for the cases wherein both goods and services are rendered one has to record fees earned proportionately.

Since fees earned is a part of the revenue of the business, it is credited to the books of accounts.

As per the Modern Rule of Accounting

| Account |

Increase |

Decrease |

| Revenue |

Credit (Cr.) |

Debit (Dr.) |

Fees Earned shall be credited as fees form a part of the revenue and as per modern rule of accounting, the increase in an income should be “Credited”.

Why is it like this?

This is a rule of accounting that is not to be broken under any circumstances.

How is it done?

For example, an accounting firm conducts a quarterly audit for various organizations. The accounting firm charges audit fees to its clients so this fee forms the revenue for the accounting firm. The fee received increases the revenue for the firm, thus, an increase in fees is credited according to modern rules.

Below is the timeline of how it would be recorded in the financial books.

Step 1 – The following journal entry for fees earned is recorded in the books of accounts when money is received. (Rule Applied – Cr. the increase in income or revenue)

| Bank A/c |

Debit |

| To Fees Received A/c |

Credit |

(Fees received from the clients.)

Step 2 – To transfer the income to the “Income and Expenditure Account”.

| Fees Received A/c |

Debit |

| To Income and Expenditure A/c |

Credit |

(Fees received are transferred to the income and expenditure account.)

As per the Golden Rules of Accounting

| Account |

Rule for Debit |

Rule for Credit |

| Nominal |

All Expenses and Losses |

All Income and Gains |

Fees earned (Income) are Credited (Cr.)

As per the golden rules of accounting for (nominal accounts) incomes and gains are to be credited. So, fees earned are credited to the financial books.

The account of expenses, losses, incomes, and gains are called Nominal accounts. Basically, nominal accounts are those accounts shown in profit and loss accounts or income statements. The balance of these accounts is always zero at the beginning of a financial year. So, fees received being a nominal account are credited to the financial books.

Example

Suppose, you are a private tutor and student students pay your tuition fees on a monthly basis. The tuition fees are income for you and according to the golden rules, fees will be credited to your books of accounts.

Below is the timeline of how it would be recorded in the financial books.

Step 1 – In the below example, the journal entry for fees received is recorded, and “Fees Received A/c” is credited. (Rule Applied – Cr. all incomes & gains)

| Bank A/c |

Debit |

| To Fees Received A/c |

Credit |

(Monthly tuition fees received in the bank account.)

Step 2 – To transfer the income to the “Income and Expenditure Account”

| Fees Received A/c |

Debit |

| To Income and Expenditure A/c |

Credit |

(Fees received are transferred to the income and expenditure account.)

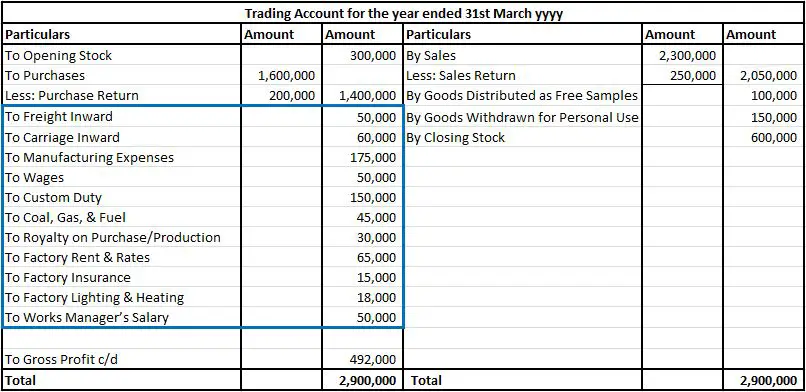

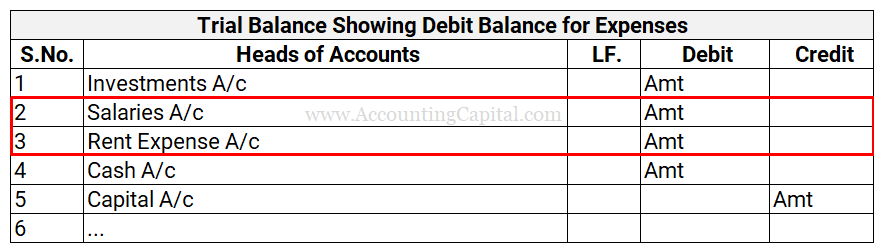

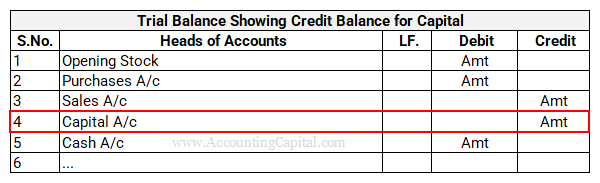

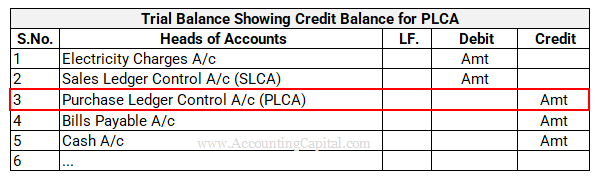

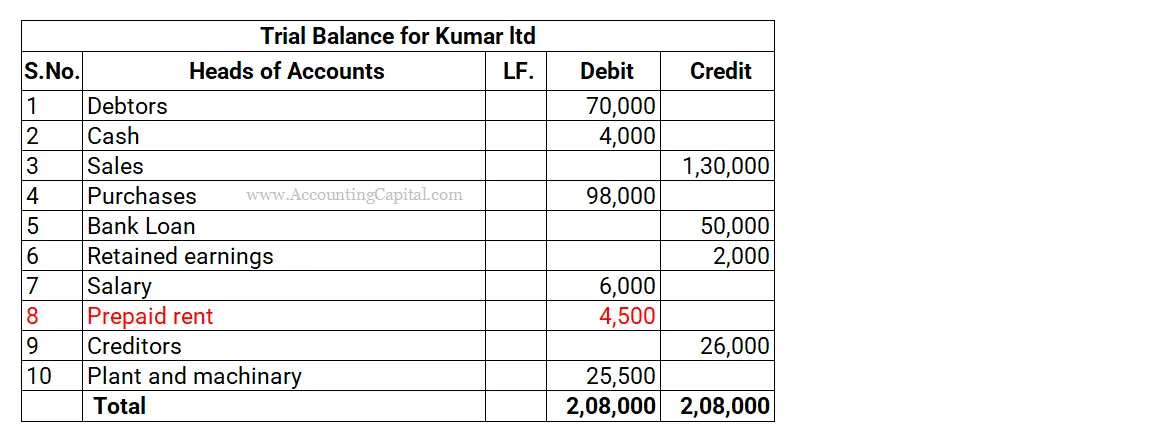

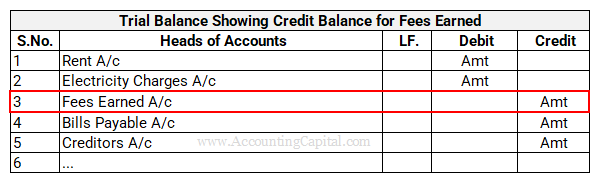

Fees Earned Inside the Trial Balance

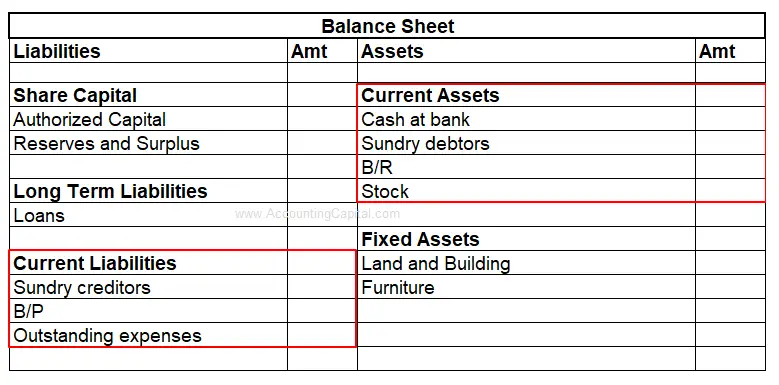

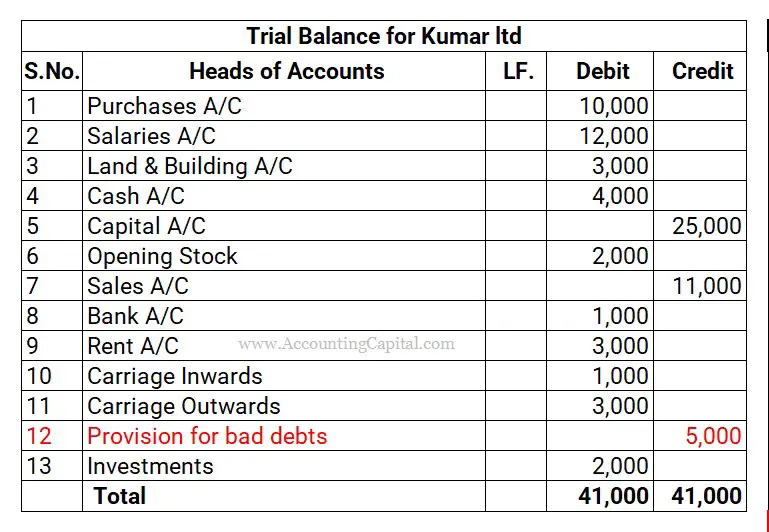

Fees earned show a credit balance in the trial balance. A trial balance example showing a credit balance for fees earned is provided below.

If an entity follows the Cash System of Accounting entire amount received shall form part of the fees earned. One need not distinguish fees based on actual earnings in the accounting period.

Journal Entry for the same shall be:

| Bank A/c |

Debit |

Debit the increase in an asset. |

| To Fees Earned A/c |

Credit |

Credit the increase in income. |

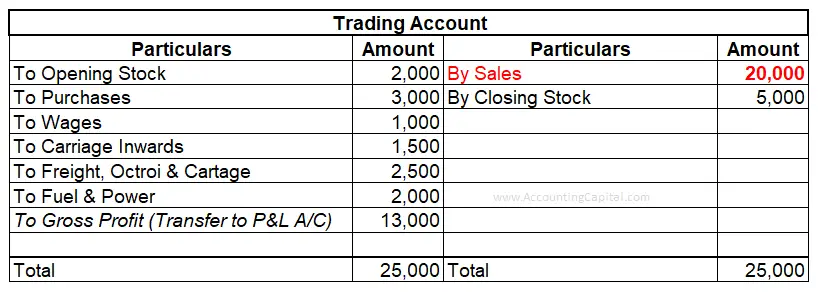

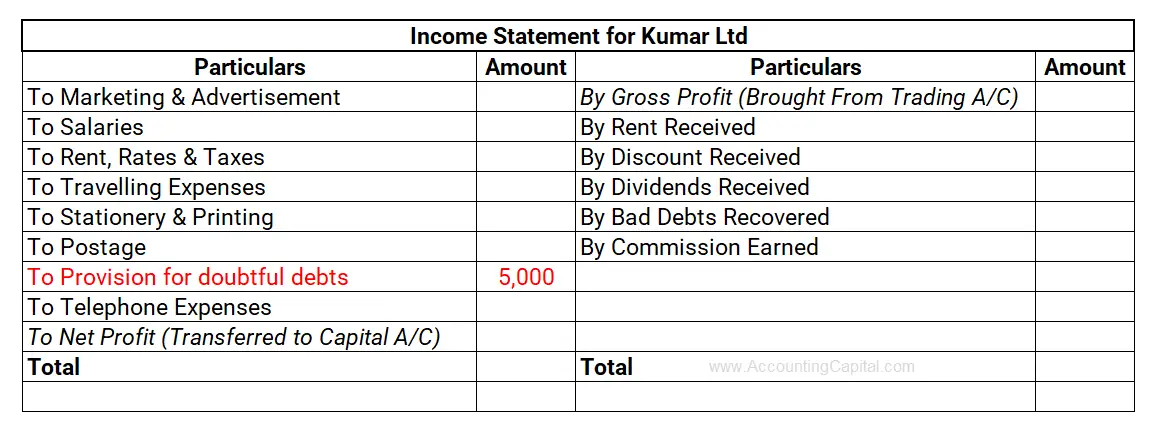

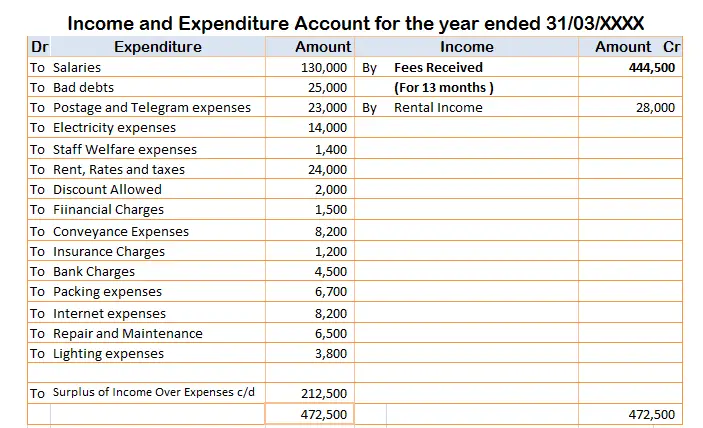

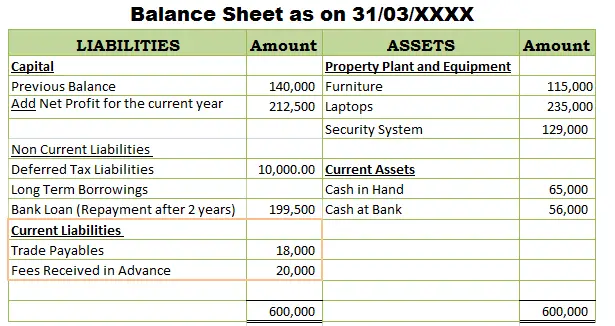

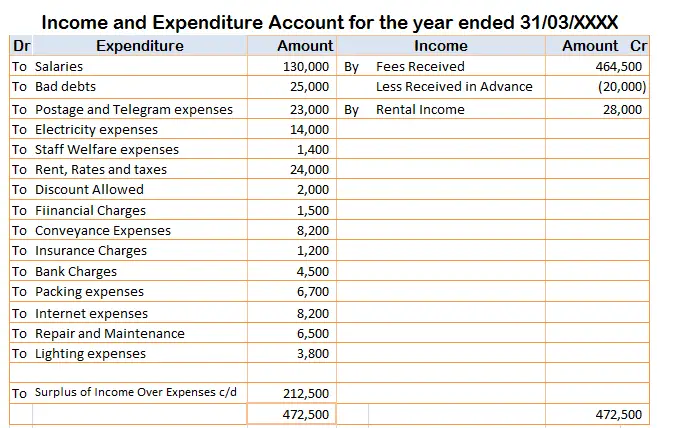

The accounting treatment in an income statement is given below;

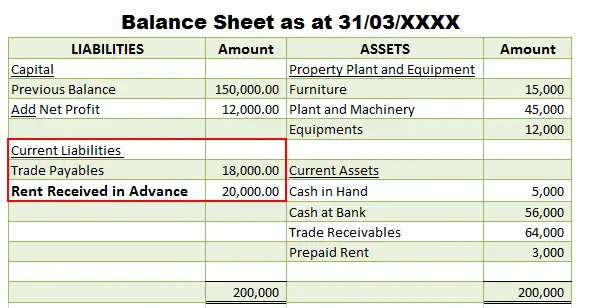

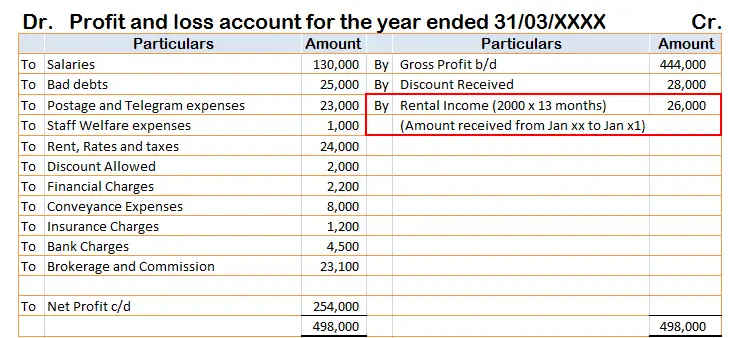

If an entity follows the Accrual System of Accounting only that part of the receipts shall form a part of fees earned which has been accrued in the reporting period.

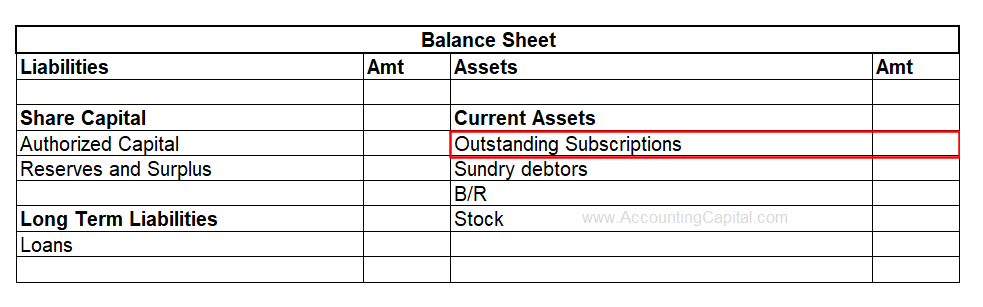

The amount if received in advance shall be recorded as a liability and if received less, then such a difference shall be recorded as sundry debtors under current assets.

Journal Entry for the same shall be;

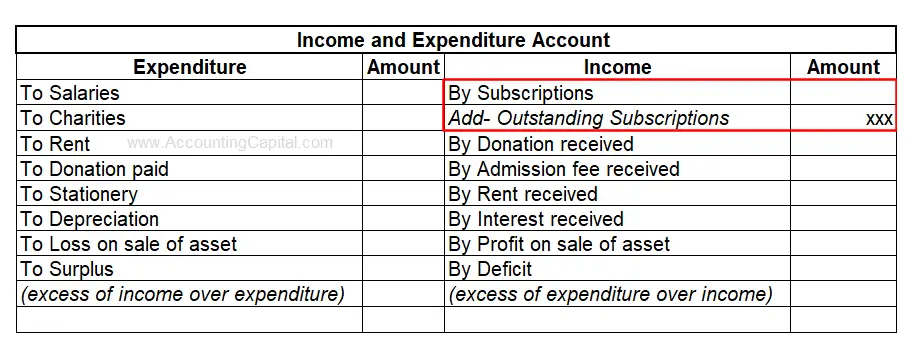

Out of the total revenue, a part of fees is received in advance-

| Bank A/c |

Debit |

Debit the increase in an asset. |

| To Advance Fees A/c |

Credit |

Credit the increase in liability. |

| To Fees Earned A/c |

Credit |

Credit the increase in income. |

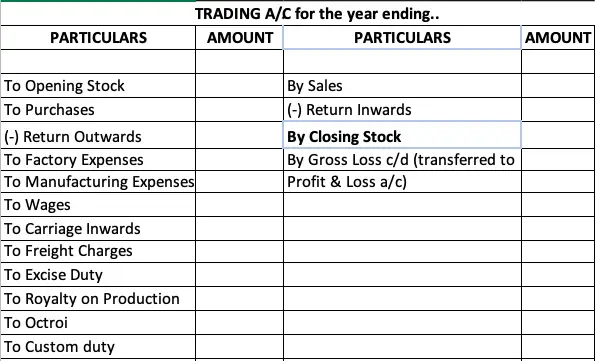

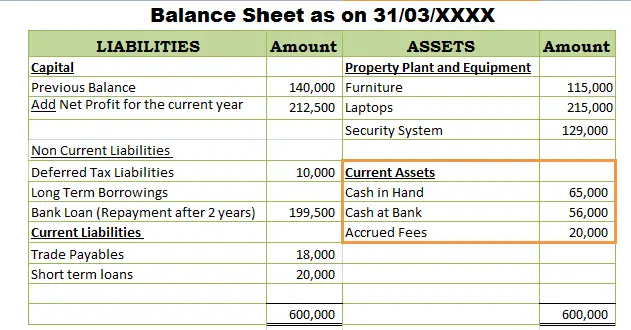

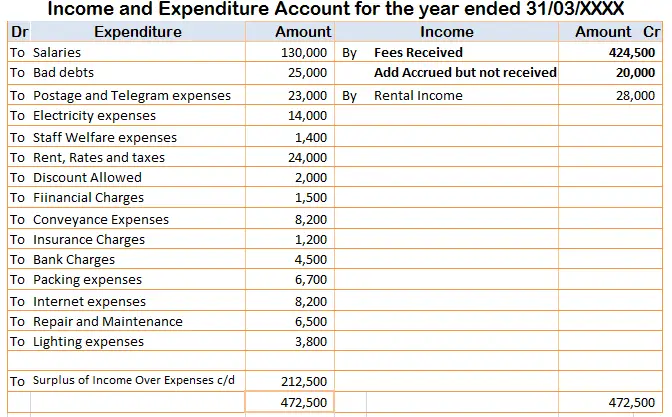

It appears in the income statement and balance sheet as;

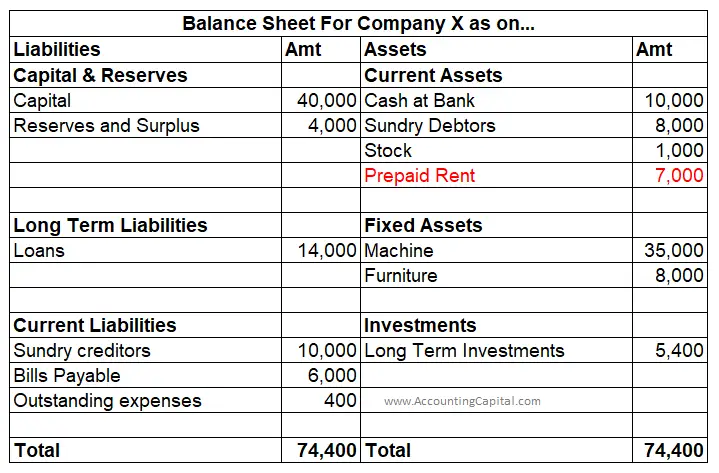

In case only part of fees earned is received in a reporting period:

| Bank A/c |

Debit |

Debit the increase in an asset. |

| Sundry Debtors A/c |

Debit |

Debit the increase in an asset. |

| To Fees Earned A/c |

Credit |

Credit the increase in income. |

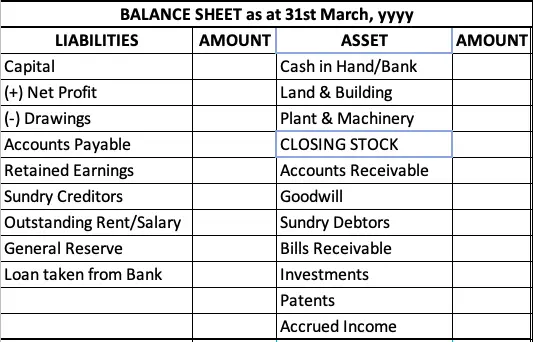

It appears in the income statement and balance sheet as –

As it can be seen in all of the cases above fees earned being an income are credited.