-This question was submitted by a user and answered by a volunteer of our choice.

In the business world, the terms “Debt” and “Liability” are used interchangeably and are understood to be the same. But in reality, they differ.

Debt

Debt refers to the money that a company borrows from external sources, typically in the form of loans, bonds, or lines of credit and it represents funds that the company owes to creditors or lenders with a promise to repay the borrowed amount along with interest over a specified period.

In other words, debt is the money borrowed by a business entity that is to be repaid to the moneylenders at a future specified date.

Examples of debt include bank loans, corporate bonds, mortgages, and other forms of borrowing used by businesses to finance operations, investments, or expansion.

Liability

Liabilities are a broader category of financial obligations that a company owes to external parties or stakeholders that include debt and other obligations such as accounts payable, accrued expenses, deferred revenue, and other liabilities that arise from past transactions or events.

Liabilities can be both short-term and long-term.

In other words, liability is an obligation to render goods or services or an economic obligation to be discharged at a future date.

For Example,

- Outstanding payment to suppliers of raw materials

- Outstanding Expenses – accrued rent, outstanding professional fees, outstanding electricity expenses, unpaid salary, etc

- Income received in advance – rent received in advance, the commission received in advance, etc

- Bills payable

- Debts accepted by an entity

Key differences between Debt and Liability

Now, let me help you understand the differences between the two terms discussed above, debt and liability.

Particulars | Debt | Liability |

| 1. Narrow/Broad aspect | Debt is an integral part of liability. It is a type of liability. | Liability is a broader term and it includes debt and other payables. |

| 2. Repayment mode | Debt can be repaid back only in cash. | Liabilities other than debt can be settled by rendering goods or services or by paying cash. |

| 3. Occurrence | Debt does not arise on a daily basis. It results only when an entity borrows money from another party. | Other liabilities arise during the course of the day to day operations of the business. |

| 4. Formal agreement | Debt involves a formal agreement between the borrower and the lender. | Liabilities apart from debt may not involve such a formal agreement between the parties. |

| 5. Utilization | Debt helps entities for business expansion and diversification. | Liabilities help entities conduct their daily business functions and processes. |

| 6. Interest payment | The repayment of debt involves payment of interest along with the principal amount. | Discharge of other liabilities may not involve payment of interest along with the actual amount of liability. |

| 7. Option of instalments | Debt repayment usually provides an option of payment in instalments. | Liabilities settlement may not provide such an option to the borrower. |

Conclusion

All debts are liabilities, but not all liabilities are debts.

Debt is under liabilities, it refers to the portion of liabilities that represents borrowed funds. Liabilities are a broader range of financial obligations, including both debt and other types of liabilities arising from various business activities.

Debt and liabilities are essential components of a company’s balance sheet and are crucial for assessing its financial health and stability.

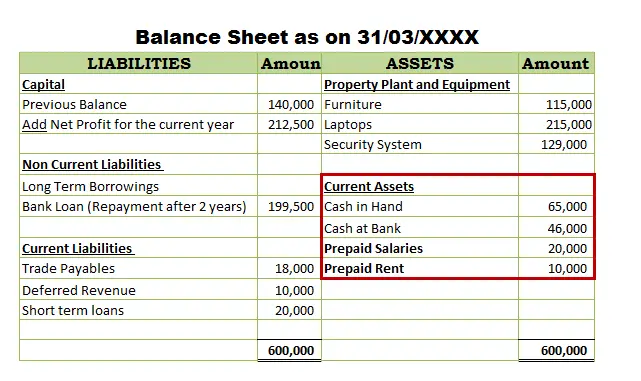

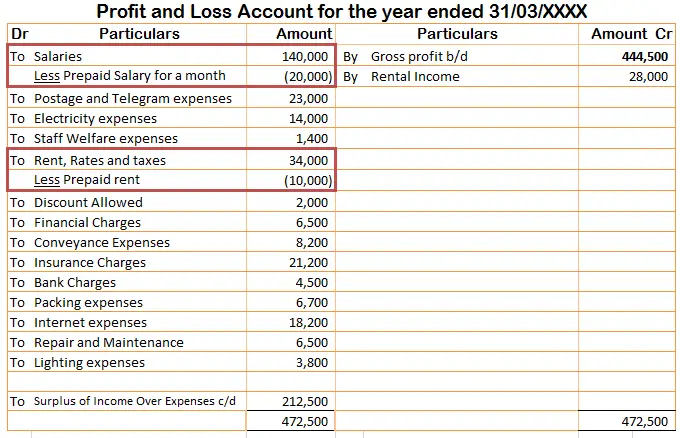

The prepaid expenses are reduced from the expenses in the profit and loss account as it is being utilized during the operating year and it slowly reduces the value of the current asset.

The prepaid expenses are reduced from the expenses in the profit and loss account as it is being utilized during the operating year and it slowly reduces the value of the current asset.