Blue Chip is a stock recognized for features such as stable earnings, high quality, less volatility and good returns. Thanks to Oliver Gingold of Dow Jones, In the early 1920s he termed such stocks as “blue chips” as he related them with the highest denomination in poker which was $25 back then for a blue coloured chip.

Such recognition helps a naive investor differentiate between “almost garbage” & a well-established firm. A regular investor with limited financial literacy can be awestruck by the number of options to invest while looking at all the listed stocks on an exchange. Let’s look at why blue-chip stocks are famous among investors.

1. Stable Earnings

If a business has stable earnings over a consistent period of time then it becomes reliable & earns the trust of investors which is considered a real good sign of a company which has its fundamentals right. If a stock has stable earnings it clearly means that the top management of the company is doing “something right” which has led them to stability. Stable earnings mean good returns for your portfolio & that remains the primary goal for all investments.

2. Dividend Payments

A solid trend which shows that the company pays dividends to its shareholders in a timely and consistent basis is a great morale booster for a stock owner simply because it acts as a cherry on the cake. It is income over and above your capital appreciation so, for example, a 20% dividend would mean an extra 20% income over and above your investment appreciation in a particular blue-chip company.

3. Strong Financials

Blue-chip companies have strong financials, for example, they are not hugely burdened by debt, their financial ratios are intact and are seen within prescribed limits, they have an efficient operating cycle etc. This leads to less volatility, minimal risk & very limited downside risk for the investor which ultimately helps them to mitigate risk keeping the entire investment profile in view.

4. Diversification

You might be someone who likes to take the risk; however, since blue-chip stocks are less risky they provide a great feature to help you reduce the entire risk profile so that even if you invest in more risky stocks which have a greater chance to fail blue chips can help you cover up some of your losses. These businesses usually have diversified business lines, demographics and multiple revenue channels which in turn help them reduce risk from operational failures.

5. Competitive Brand Advantage

Most of the blue-chip companies have a stronghold and their presence can be felt in daily lives of common people, for example, if you buy a can of sprite then you are adding up to the revenues of coca-cola if you buy ahead & shoulders shampoo you are adding up to the revenues of P&G. There are many such examples where it can be seen that blue chips get a competitive advantage due to their cost efficiency, franchise value, goodwill or distribution control.

These are the top 5 among various reasons to invest in blue-chip stocks.

CRE (Commercial Real Estate) is also called Commercial property, investment property or income property. It is mainly related to all real estate which is used for business purposes to generate income. Examples of such real estate include shopping malls, restaurants, business offices, hotels etc.

Commercial real estate includes any type of property or vacant piece of land which fetches or has the potential to fetch income. From a business point of view, commercial real estate is any kind of commercial space that can be leased (or at times bought) for the use of operating a business. A commercial real estate (CRE) is usually leased and the owner collects a monthly or yearly payment in lieu of its usage by the tenants.

It can be categorized into a different type of property such as if it is a mall then the property falls under retail type, here is a quick look on the top categories:

Retail

Leisure

Offices

Industrial

Healthcare

*Residential

Few of the top known real estate landlords of the world are CBRE Group, Knight Frank, GE capital real estate, AMB Property, Prologis, Simon Property Group, Agile Property, General Growth Properties, ING Clarion, LaSalle Investment Management, RREEF, DLF, EMAAR etc.

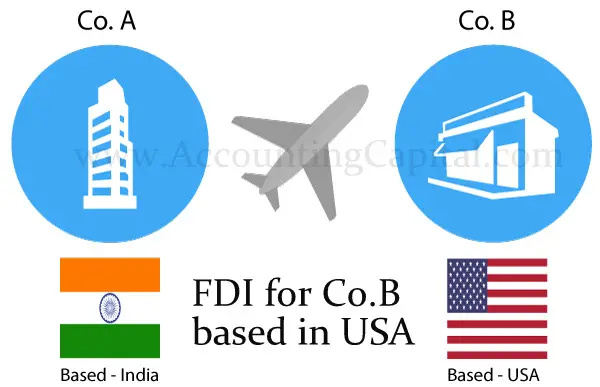

FDI stands for Foreign Direct Investment. When a company from a particular country invests in another company based in a different country in a way that it acquires some (generally 10% as per OECD) controlling stake is known as Foreign Direct Investment.

Like in the example info graphic shown below, Company A from India invests in Company B based in USA such an investment is termed as FDI (Foreign Direct Investment). The investment can happen in form of buying tangible assets, controlling stakes in ownership etc. FDI is not only a transfer of ownership as believed but it is also transfer of elements complementary to capital including technology, management and skills. FDI helps developing nations by filling in investment gaps which the domestic investors & the government can not fulfill on its own.

FDI (Foreign Direct Investment) is different from FPI (Foreign Portfolio Investment) which means holding of shares and other financial assets by foreign investors without any controlling, management or ownership rights over the company, FPI is a indirect investment whereas FDI is direct.

There are 2 primary ways to invest in FDI:

Cross border M&A (Mergers & Acquisitions) which means buying controlling stake in a foreign company (Brownfield Investment)

Extending company’s operations to foreign and begin building new factories & offices from scratch (Greenfield investment)

Importance & Types of Foreign Direct Investment

1. Increased FDI implies rise in economic development because of increased capital and increased tax returns for the host country.

2. New projects are channelized to hike development by FDI investment in host countries.

3. Tough competition leads to highest efficiency and productivity levels in host country.

4. FDI results in specialization of skills and creation of new jobs.

5. FDI also generates employment opportunities created by different entities, for local countries.

Top reasons to invest in foreign companies are:

Tap new markets

Skilled labor

Cut down costs

Other strategic profit making decisions

Type 1 – Horizontal FDI

If a company lets say a e-commerce company expands its business in another country however still does the same thing both at home and abroad it is knows as Horizontal FDI. So in this case the e-commerce company enters a new geographical territory but the operations remain exactly the same.

Type 2 -Vertical FDI

When a company lets say an e-commerce company either moves upwards or downwards related to its operational cycle adding value to its business cycle it is called vertical FDI. A good example of this will be the same e-commerce company (who already has established business in a foreign country) acquiring a controlling stake in a logistics company.

You can be an entrepreneur who is running a start-up, a home-based business or a small firm that is trying to make a mark. While playing the lead in this role of your life you are wholly responsible for your actions i.e. generating income, profits, paperwork, legal requirements, taxes etc. No matter what you do you can’t fully escape from paying taxes but you can definitely work towards reducing your tax bills. Don’t confuse Tax evasion with Tax avoidance, where the former is totally not suggestible the latter helps you to pay the least amount of tax legally. Just be very sure with your facts and ensure to never mess with the IRS.

Home Office Deduction

The cost of the workplace where you conduct your business either if you rent or acquire it, can be deducted as a home office expense. Your declarations are considered as final and considered true while filing taxes so it is always a good suggestion to be honest and always have supporting facts in case if you are examined. It is considered as a complex deduction, hence IRS gives 2 different ways to get this done, Standard Method and Simplified Method.

The tax deduction includes expenses such as interest on mortgage, insurance, utilities, repairs, depreciation and maintenance charges which are paid during the year. For example, if your workspace is 30% of your home, then 30% of your power bill for the year is tax-deductible. The standard method needs you to calculate your actual home office expenses whereas the simplified option lets you multiply an IRS-determined rate by your home office square footage.

Travel Expenses

An expense qualifies to be categorized under this head if it requires you to be away from the vicinity of your tax home, usually for longer than 1 workday & requires you to eat, rest and sleep to meet the demands of your work while travelling. Also, this type of travelling has to be business-related where you are expected to be involved in only business-related activities such as attempts to gather new customers, gain new skills, important conferences etc.

Travel expenses that can be covered are transportation, meals, telephone, baggage and shipping, cleaning, tips etc. You must keep complete and accurate records of your business dealings as it may be asked for proof. Tax expense which will be deducible includes the transportation cost to and from, tickets, lodging, meals. Full 100% travel expenses related to the business are deductible but in case of meals and entertainment deduction is limited up to 50% of the actual cost, if you keep the records. Or it can be calculated by 50% of the standard meal allowance. Whereas, on entertainment, the IRS has numerous restrictions. If your entertainment expenses qualify for the test, it is only 50% deductible. You must keep a record of all receipts relating to tour, entertainment and meals.

Click Here to see detailed deductions on Travel, Entertainment, Gift, and Car Expenses on IRS’s website.

Click on the Image to See More Credits and Deductions on the official IRSWebsite

Telephone & Internet Charges

These charges refer to calls made & the internet used for business purposes. The common idea is to only declare deduction of the consumption that happens related to business operations, so for example if 40% was used for the business then only 40% of total charges should be claimed for deduction.

You may or may not have a separate line for your business, in the latter case when you receive your telephone bill each month you can highlight the business calls and file it accordingly. Many people carry a cell phone, especially for business calls. They can claim the full bill as tax-deductible. It is highly advisable to NOT to include your personal usage.

Insurance Premium

There is no business without the owner so your personal health insurance can be used as a deductible under tax laws. Whatever the amount, you can use all of it except that it cannot exceed more than the net profits of your business. You may deduct premiums that you paid to provide coverage for your spouse, dependents and your children who were below 27 at year-end, even if they are not your dependents. It can’t be claimed if you pay a different type of insurance premium, either single or jointly, such as the one offered by your spouse’s medical plan.

Two important points must be kept in mind:

1. Employment of your spouse must be real.

2. Any kind of failure in meeting these requirements may result in a court situation.

Car Mileage

When your car is used for business purposes, those expenses are tax-deductible. Make proper records of such trips and do not mix it with personal trips. The deduction can be taken out using two methods:

1. Standard Mileage 2. Actual Expense Method

Standard Mileage: This method is the easiest because it requires record keeping and minimal calculation. Write down the dates and the miles you drove your vehicle for business purposes. At the end multiply your annual miles by standard mileage rate which is 57.5 cent per mile. The answer will be your tax-deductible amount.

Actual Expense Method: For this, the percentage of business driving must be calculated for a full year along with operating charges such as gas, registration fees, repairs and insurance. Now let us say you spent $4000 as operating expenses and used your car for 10% business purposes, the result would be $400 as a deductible expense.

Don’t forget to keep track of your mileage. While you can’t deduct all of your mileage, you can deduct mileage that is work-related and outside of your normal commute, so you’ll want to keep track of that throughout the year says Troy Martin, a Utah CPA for Cook Martin Poulson, P.C.

Bonus – All in One Deduction

All contributions to Simplified Employee Pension – SEP -IRA, Savings Incentive Match Plan For Employees Of Small Employers – SIMPLE & Independent 401(K) are tax deductibles and help you reduce your taxable income. Why do we call them cherries on the cake is because they not only help you save tax but they also help you attain tax-deferred investment gains for later on. This year (2015) the contribution limit for Independent 401(k) has been increased to $53,000.

Small business owners’ tax deductions are quite complicated. But the above overview gives clear information about the aspects which will be helpful in a tax deduction. You may take the help of a professional in case if you don’t wish to get into all the related hassle. While we encourage you to avail all legal tax deductions for small business owners we would also like to remind you that illegal tax evasion can lead you to heavy penalties or jail time.

RBI stands for Reserve Bank of India & it is headquartered in Mumbai, Maharashtra. It is the Central Bank of India, controlling monetary values. It came into being on 1st April 1935. On 1st January 1949 RBI was nationalized. The share capital was divided into 100 shares owned by private shareholders, however now shares are held by the government. RBI’s central office was in Kolkata, Now it is in Mumbai from year 1937. It manages loans and its terms and controls the liquidity of funds in market. Reserve Bank of India is a member bank of ACU and topmost member of Alliance for Financial Inclusion (AFI).

Dr. B. R Ambedkar wrote about RBI in his book- The Problem of Rupee- Its origin and its Solution, in presence of Hilton Young Commission. The Foreign Exchange Management Act came into being in June 2000. RBI enforced nationalized banks with capital markets, developed economic growth in spite of barriers in late 1990′s .

Structure of RBI

Board of Directors (BOD) It is the central committee of central bank. Board of Directors are appointed for a term of 4 years. It consists of 4 Deputy Governors, 4 Directors from Ministry of Finance and 10 other Directors.

Governors Raghuram Rajan is the governor of RBI. The other 4 Deputy Governors include HR Khan, Dr Urjit Patel, R Gandhi and S S Mundra.

Supporting Cast RBI has four regional representatives; New Delhi in North, Chennai in South, Kolkata in East and Mumbai in West. Five members form the representation.

Branch and Office It has 4 zonal offices and around 19 offices in following states and cities: 1. Ahmedabad 2. Chandigarh 3. Bhopal 4. Delhi 5. Mumbai 6. Nagpur 7. Jammu 8. Kolkata 9. Patna 10. Lucknow 11. Srinagar 12. Simla

Functions of RBI

1. Manager, Regulator and Controller of Financial Market:

RBI is the supervisor of financial system as it maintains public faith in this system, provides transparency in its activities and protects the interest of investors.

2. Exchange control manager:

RBI facilitates internal and external trade and equates the balance of payment account. It also helps in the growth of foreign exchange market in India.

3. Issues Currency:

Reserve Bank of India issues and exchanges currency, both notes and coins as per the circumstances. It sells and purchases securities to maintain the price stability and liquidity of assets.

4. Banker’s Bank:

It serves as a bank to commercial banks where they can deposit money to balance the monetary structure of economy. By providing advances to commercial banks, it acts as lender of last resort.

Rates and Ratios

As per January 15, 2015 , the rates are:

1. Bank Rate – 8.75% 2. Repo Rate – 7.50% 3. Reverse Repo Rate – 6.75% 4. Cash Reserve Ratio – 4% 5. Statutory Liquidity Ratio – 21.50% 6. Base Rate – 10.00% to 10.25% 7. Savings Deposit Rate – 4% 8. Term Deposit Rate – 8.00% to 9.00%

On September 5th 2005 with assent of the president of India a new policy came into existence which worked towards providing livelihood security in rural areas of India. It started with the name “NREGA” which stood for National Rural Employment Guarantee Act and then an additional letter “M” was prefixed making it “MNREGA” Mahatma Gandhi National Rural Employment Guarantee Act. MNREGA is an employment scheme which provides social security by guaranteeing a minimum of 100 days paid work per year to all the families whose adult members opt for unskilled labor-intensive work.

History

After three years of observation, the government launched schemes like Jawahar Rozgaar Yojana, Food for Work Programme, Sampurna Grameen Rozgaar Yojna. These acts were predecessor to Mahatma Gandhi National Rural Employment Guarantee Act, which was a legal title. This act was firstly initiated in Maharashtra in 1970’s by Former Chief Minister of Maharashtra Vasant Rao Naik. NREGA act resulted in a boon for millions of farmer families. This act was accepted by Planning Commission and later on accepted nationwide. Such acts gave lessons to government regarding ‘Rural Manpower Programme’ ‘Crash Scheme for Rural Employment’ ‘Drought Prone Area Programme’ ‘Marginal Farmers and Agricultural Laborers Scheme’. Keeping the objectives of wage employment, production of valuable assets and food security still, the government focuses on implementing new schemes by seeking drawbacks of old ones. MNREGA is one of the outcomes of same.

Key Features

1. To provide job security to all adult members for at least 100 days in a financial year 2. To create permanent wealth such as roads, ponds, wells. 3. Employment is provided within a range of 5 kms from residence of applicants. 4. Minimum wages will be provided. 5. Applicants will be given unemployment allowances, if work is not provided within 15 days of application.

Highlights

1. By 1st April 2008, this act covered all districts of India. 2. ‘Stellar Example of Rural Development’ is what World Bank termed this act, as per World Development Report 2014. 3. This act is executed by Gram Panchayats. 4. Labor-intensive tasks are preferred. 5. Women empowerment, environment protection, boosting social equality are the areas covered under NREGA act. 6. The act safeguards the effective and efficient management and implementation of its policies. 7. The act also ensures a genuine, transparent regulation of its activities.

MNREGA has been criticized for making agriculture less profitable as landless laborers are lazy and they don’t want to work on farms as they can get money without doing anything through minimum money guarantee at NREGA work sites.

A thing, person, or quality which is useful or beneficial is termed an asset. In the financial world, assets are things tangible or intangible that hold an economic value and are held by businesses to extract future benefits. Their value is adjudged by the amount they can fetch in monetary terms & that number is further used in the appropriate column of a company’s balance sheet.

Examples of assets – Cash, machinery, stock, building, vehicles, receivables, copyrights, patents, logos, etc. They can be classified as Current, Fixed, Tangible, Intangible etc.

In Simple Terms – An asset is a piece of property that is valuable and useful. It is a thing that has economic value and can be utilized by businesses to generate income in the future. Its value is judged by how much money it can be sold for. A company’s balance sheet shows the value of an asset.

Example

A firm bought a new printer for official purposes priced at 1,00,000. The printer, in this case, is an asset to the business and the amount to be booked in the balance sheet will be 1,00,000. This is a tangible asset which is subject to depreciation, unlike an intangible asset which is amortized.

Short Quiz for Self Evaluation

Loading

Your quiz has been submitted

Want to re-attempt? - Simply “refresh” this page.

Please check out more content on our site :)

Subscribed? - Check your mailbox

Thank You!

Server Side Error

We faced problems while connecting to the server or receiving data from the server. Please wait for a few seconds and try again.

If the problem persists, then check your internet connectivity. If all other sites open fine, then please contact the administrator of this website with the following information.

NEFT stands for National Electronic Funds Transfer. It’s an electronic payment system of India facilitated by RBI (Reserve Bank of India), it helps people with one-to-one money transfers. People using this facility can transfer money electronically from any branch of bank to any other individual or organization within the country that has a bank account which has NEFT service enabled.

Not all bank branches of the country are part of NEFT funds transfer network. The branches which are NEFT-enabled, only those can become a part of this network. The consolidated list of bank branches which are a part of NEFT, can be found by clicking here. You can select the appropriate option on this link.

Limits, Charges & Operating Hours of NEFT

Limits

The amounts carry no restrictions. But the cash based transactions are limited up to a maximum amount of INR 50,000/ Per Transaction for cash based payments.

Charges

There are no charges to receive money, however to send money following charges are applicable,

0-10,000

INR 2.50 + Service Tax

10,000 – 1,00,000

INR 5.00 + Service Tax

1,00,000 – 2,00,000

INR 15.00 + Service Tax

2,00,000 Above

INR 25.00 + Service Tax

*In some cases it may not attract any charges example salary accounts, specially designed accounts, No frills etc.

Operating hours

Weekdays (Mon-Fri)- 8 a.m to 7 p.m (twelve settlements) Weekends (Saturday)- 8 a.m to 1 p.m

Who all can transact through NEFT?

Any individual, association or firm having accounts with banks can transfer money through NEFT. Even people who don’t own an account (walk-in-customers) can deposit money in NEFT enabled banks, adhering to instructions. Such customers are required to supply full information regarding their address, telephone number, supplement accounts and much more.

Only the individuals, firms or associations which hold accounts with any branch of bank can receive payments under NEFT system. So it becomes mandatory for the beneficiary to hold an account with the NEFT enabled bank.

There are no geographical restrictions on the banks. The transactions can be carried out from anywhere to everywhere within the country.

Working of the NEFT system

The operating of this system can be understood in following steps:

Step 1: An individual or the association desiring to transfer funds through NEFT, need to execute/complete the application form consisting details of beneficiary such as name, address, bank branch, account number and the money to be deposited. The form is available at the commencing bank branch. Even ATM offers this facility for some banks.

STEP 2: A message is prepared and sent to the NEFT Service Center (also known as pooling center) by the commencing bank.

STEP 3: That message is dispatched by pooling center to the NEFT Clearing Center, which is managed by National Clearing Cell, Reserve Bank of India, Mumbai.

STEP 4: The funds are sorted by Clearing Center as per the bank branches from commencing banks to destination banks. And after that those messages are delivered by the pooling centers of the destined banks.

STEP 5: The messages are received from the Clearing Center to the destination banks and they approve the request against the beneficiary customers.

For more detailed information on NEFT you can visit www.rbi.org.in

A stock exchange or a stock market acts as a service provider, it is one stop shop for traders to buy or sell financial instruments such as shares, bonds etc. A stock exchange can be approached for both issue and redemption of Publicly listed shares. To be able to trade on a stock exchange you’ll need to have a trading account. SEBI (Securities Exchange Board of India) is the governing body in India that acts as a regulator of capital markets under a resolution of the Indian Government.

Leading Stock Exchanges of India are NSE (National Stock Exchange) and BSE (Bombay Stock Exchange)

WHAT IS BSE?

Bombay Stock Exchange is the expansion of term BSE. It is an ancient stock exchange of Asia, incorporated in 1875 and it is headquartered in Maharashtra (Mumbai), India. Bombay Stock Exchange is the 10th largest stock exchange in market capitalization. Around 5400 companies are listed on BSE as of 2015. Not many know that BSE started under a banyan tree with the total money used back then were INR 7.

Key Features of BSE

CEO/MD – AshishKumar Chauhan

Market Capitalization – USD $1.7 Trillion

Currency Traded – INR

Name of Indexes – BSE Sensex, BSE Mid Cap, BSE Small Cap, BSE 500

ISO Certified – Yes, first one to get this certification

Timings

09:00 to 09:15 – Pre-open trading session

09:30 to 15:30 – General trading session

17:05 to 17:15 – Position transfer session

17:05 to 17:55 – Closing session

17:07 – Option Exercise session

OBJECTIVES OF BSE

From more than 130 years, BSE is providing an effective and efficient capitalization platform. It provides a transparent electronic screen based market for trading in different securities, instruments, funds and bonds, be it small or medium enterprises. It also serves as host of secondary services for investors like risk management, market facilities, education. These services, processes safeguard the investor’s interest, develop Indian Capital Market along with innovation and competition. It also provides various depository services. Also BSE acts as a regulator, which provides surveillance mechanisms through which all the speculations, irregularities and manipulations can be detected.

WHAT IS NSE?

National Stock Exchange is the expansion of term NSE. It is the top exchange in India by number of trades in equity shares and number three in the world. It is situated in Mumbai and was established in November 1992 as Taxation Company. It was accepted as stock exchange in April 1993 under the Securities Act 1956, with P.V. Narasimha Rao being the Prime Minister of India and Manmohan Singh being the Finance Minister. NSE has around 1600 listings as of 2015.

Key Features of NSE

CEO/MD – Chitra Ramkrishna

Market Capitalization – USD $1.65 Trillion

Currency Traded – INR

Name of Indexes – CNX Nifty, CNX Nifty Junior, CNX 500

Location – Bandra, Mumbai

Timings

09:00 to 09:08 – Pre-open trading session

09:15 to 15:30 – General trading session

OBJECTIVES OF NSE

The key objective of National Securities Exchange is to provide a transparent trading system for all kinds of securities worldwide. It also protects the interest of investors. It achieved its objectives in quite short span of time. Many new terms have come into being to give a variety of options to investors.

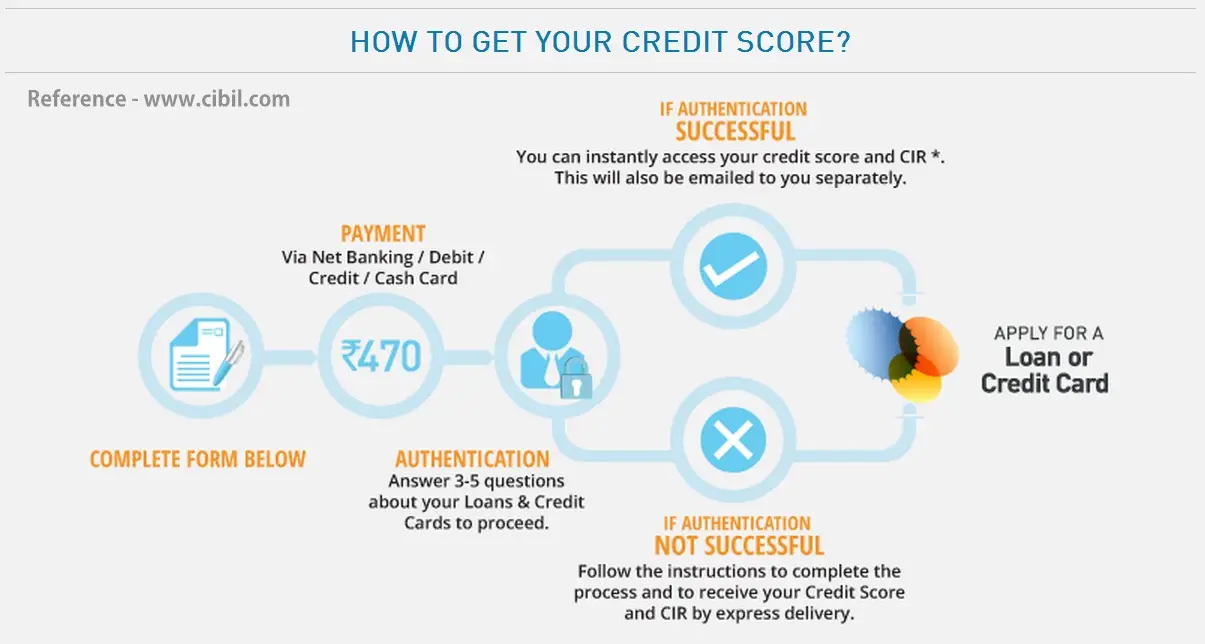

Whether you’re applying for a consumer loan, home loan, credit card, auto loan or just interested in having a look at your CIBIL report, your credit score will play a vital role in the process. CIBIL can be elaborated as Credit Information Bureau India Limited and it keeps all records of your loans, credit cards and other forms of considerable credit. How would you get your CIBIL credit score?

Step-by-Step Guide

You need to start by filling out a form on CIBIL’s website, you can Click Here for the form. This form required you to fill in personal details including demographics, ID Proof, Address Proof etc.

CIBIL TransUnion Score (CIR – Credit Information Report will be included), this in entirety will cost you INR 470, After filling the form as per the previous step you will be required to make a payment through either CC/DC/Cash Card or Net Banking.

Now you will be authenticated to ensure and identify that your request is valid and the correct person is requesting it.

If authenticated successfully you will get immediate access to your credit score and CIR online.

or

If authentication fails, you will get be given a set of instructions to complete and after that you will receive your credit score and CIR by express courier.

Can You Get Your CIBIL Score for Free?

No! you as an individual can never get your credit score for free, banks might get it and they will usually not share the scores with you. If you are being denied of credit cards, loans etc. recently it is a good sign that your CIBIL score has been hit hard & needs fixing. One distant possibility is a free credit score being offered with some financial or a similar product as a promotional offer. INR 470 is the cost you’ll need to incur as of 2015.

What are Bad & Good Credit Scores?

Scores would range somewhere between 300 and 900, you can say that is how CIBIL TransUnion judges you on your repayments. You can refer to the below list to understand more about what your credit score spells for you.

Heard about Public Provident Fund (PPF), but don’t know much about it? For details, have a look at the explanation.

WHAT IS PPF?

Much known as Public Provident fund, PPF a savings instrument introduced by the ministry of finance in India which also helps in tax savings. In 2015 this scheme is more than 45 years old and is still among the top financial instruments used for tax planning. PPF is a success not only because it provides decent returns on investment but the money invested also gives tax benefits. The returns are usually higher than what the Fixed Deposits offer. It is a Long Term Debt Instrument of Indian Government. Post Offices as well as some Banks gain the authority to access PPF accounts.

Eligibility

A person needs to be ROI (Resident of India)

Non Resident Indians (NRI’s) cannot advance money in Public Provident Fund.

Minors are eligible to open an account by their legal guardian.

PPF account can not be opened under the name of HUF (Hindu Undivided Family)

Documents Required

Pan Card copy

Form A (Opening Form)

Passport size photo

Any residential proof

Investment Amounts

The minimum and maximum limit every year for investing in public provident fund is INR 500 & 1.5 lakhs respectively, deposits may be made in monthly installments (max 12/year) or in one go. Any deposits above the specified amounts will not fetch any interest income. Failure to deposit 500 INR would make you liable for a penalty.

Interest Rates and Other Benefits

RBI declares the Interest Rate every year in March. For 2014-2015 this is 8.70%, which was exactly the same as previous year.

It is advisable to invest money in this account before 5th of each month to gain maximum returns, as the interest is calculated on the least balance from 5th to the last of month. Therefore, it is desirable to deposit additional sum before time to earn additional benefits.

Also the entire sum of 1.5 lakhs can be advanced before 5th April to earn interest on the entire amount for the whole year.

Duration, Loans & Transfers

From the day a PPF account starts, it’s accessible till 15 years. After 15 years, the tenure ends. On the expiry date, the money can be withdrawn. Also, the account holder can opt for extension of account up to a maximum of 5 years with adherence to certain terms and conditions.

Loans are available to individuals from third financial year itself. All such loans are to be reimbursed within months. disbursed amount can not be more than 25% of balance at the end of 2nd immediately preceding year. If you have paid the first loan successfully and you are between 3rd and the 6th year you may be available for a 2nd loan.

The accounts of individuals can be easily transferred to Post Offices or other Bank Branches free of charge.

Benefits Regarding Tax

Such benefits come under SEC 80(c) of IT ACT. The amount deposited in PPF account, is divided into two parts.

PRINCIPAL AMOUNT which is the total sum which you invested

INTEREST AMOUNT which is the benefit you will get on the above investment

Tax benefit includes benefits on both the amounts, up to a maximum of INR 1,50,000

ON PRINCIPAL AMOUNT

This amount can be reduced from the actual Income Tax amount of that year. The sum so arrived is liable for tax payment. It can also be reduced from Wealth Tax.

ON INTEREST AMOUNT

The return, in form of interest is tax-free. No tax formality is incurred on the interest amount.

Policies Governing PPF

Only one account is accessible by an individual. Except in case of minor, if second account of a person is disclosed, the principal amount will be handed over back to him but the interest thereupon will be cancelled.

A PPF account is not a joint account. A nominee can be selected, who will be benefited after the death of account holder.

In case, no nominee has been appointed, the benefits will be given to the legal heir’s of the deceased account holder.

PPF Disclaimer

By default, the PPF account will be deactivated, if no investment is made in the whole year.

A penalty of 50 INR is to be borne by the account holder for again activating the account along with 500 INR for the inactive year.

The deceased account cannot be continued by the nominees.

The identity of legal heirs or nominees is just in case the balance in deceased account exceeds 1.5 lakhs.

PPF Vs Some other Schemes

Tax Savings Fixed Deposit

PPF and Tax Savings Fixed Deposit both are deductible incomes.

But the tenure of Tax Savings Fixed Deposit is 5 years, which is less when compared to PPF.

Even the benefit earned on Tax Savings Fixed Deposit is taxable which is the reverse of PPF.

National Savings certificate

Both schemes include deposits made in Post Office or Bank Branches.

NSC is a scheme which involves deposit only once whereas PPF requires deposit every year.

The tenure of NSC is 5-10 years whereas that of PPF is 15 years.

You need funds to start a new venture? or Require money for education of your children? or Maybe you’re looking out for a new credit card or loan to buy a new car/house? Whatever the requirement, you will need to choose between Secured or Unsecured debt. Each type has its own positives and negatives. So it’s better to be aware about them by going through our cover story.

WHAT ARE SECURED LOANS?

Secured loans are those loans which are backed by some or the other kind of property or assets. The word secured depicts that these type of loan are protected by some collateral. In case if a borrower fails to pay the loan the creditor can legally auction or sell the collateral to recover the original amount disbursed. Assets such as home, automobile, stocks, gold etc. can be used as collateral. The title of the pledged article will be held by the loan provider (creditor) until it is repaid in full along with the interest. A secured loan is generally less costly for the debtors and more peace-of-mind oriented for the creditors.

Examples of Secured Loans

Home Loans

Construction Loans

Gold Loans

Car Loans

Boat Loans

PROS AND CONS OF SECURED LOANS

PROS

Secured loans are available for larger amounts as compared to personal loans.

Less paper work and easy to qualify if one has suitable collateral against the loan.

The time period of loan repayment is also higher as compared to other type of loans.

Such loans offer lower interest rates as they are secured against your property.

CONS

Failure to repay the loan would result in losing your property.

Few secured loans have varying interest rates that could make your repayment amount higher.

Secured loans bear risk factor because they need expensive collateral security.

You may incur high penalty fees on the repayment of loan.

WHAT ARE UNSECURED LOANS?

Unsecured loans are totally opposite to secured loans, they are disbursed without a collateral in place. Such loans are accessible to anyone & you need not have a suitable asset to be pledged as a collateral. Taking unsecured loan implies that the borrower can repay through his financial resources itself. Unsecured loans are usually more costlier than secured loans due to no security in place and more prone to end up as a total loss to the creditor. If you fail to pay an unsecured loan, the lender can drag you to court and damage your credit worthiness as well.

A borrower is judged by 5 C’s before a secured loan is provided:

Character

Capacity

Collateral

Capital

Conditions

Examples of Unsecured Loans

Credit Cards

Education Loans

Personal Loans

Renovation Loans

PROS AND CONS OF UNSECURED LOANS

PROS

Such loans are quite cheap as compared to Secured ones.

They give number of options to choose the repayment mode.

You will not lose any of your assets.

All you need is a document and signature and you can avail this loan

CONS

As no property is mortgaged, the lenders charge higher interest rates even for a short-term.

You can get only a limited sum of money from lenders as they give more money on secured loans because there the financial risk is secured.

Since the loan amounts are not large, the repayment periods are also short as compared to repayment period of secured loans.

One may get trapped into the debt cycle due to continuous non-payment of loan amounts

WHICH ONE IS BETTER?

The truth, there is NO right answer to this question. What, When, Which & How to opt for which type of loan, totally depends on your need of taking the loan. Both are a good option if they fit in to your requirements perfectly. Generally secured loans are good from creditor’s point of view as there is a collateral to cover up the losses, whereas an unsecured loan is good from a applicant’s point of view as he/she would have no tangible asset to lose in case of a default.

The key is to think in the right direction before applying for the loan. Auto, education, personal, consumer etc. all these type of loans are designed specifically for the purpose stated in their respective name(s). Be willing to pay more & quicker in case if you don’t wish to collateralize your loan. So the preference solely depends on your requirement.

Once you are clear about the type of loan you require, you must approach different lenders to see what interest rates they offer. Don’t forget to compare the rate of interests being offered by different banks and NBFCs before you finalize your lender. Try to browse through some websites to check their respective USPs & repayment plans. Cross check and apply for a loan with the lender which suits best, according to your requirements.

The direct entry route takes you directly to the intermediate stage of the course, meaning skipping the CA Foundation exam.

The candidates who are eligible to register themselves with the Direct Entry Route are given below –

Commerce Graduates / Post Graduates scored minimum 55% marks or other graduates or Postgraduates who scored minimum 60% marks.

Candidates who have passed the Intermediate level of Institute of Companies Secretaries of India or Institute of Cost Accountants of India.

Direct Entry Course details can be seen on the following link.

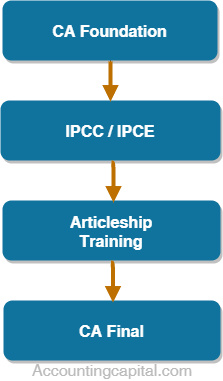

CA Foundation course route has a total of Four Major steps, this flow chart will help understand it better.

Direct entry course, on the other hand, reduces the first step and gives direct entry to the aspirants to the next level. Eligibility can be checked along with other criteria(s) for both the entry types at the following link.

Stage 1 – CA Foundation (Previously CPT)

CA – Foundation is the first stage of CA course. It comprises of four subjects. A candidate is required to secure at least 40% marks in each subject and a total of 50% in aggregate to clear this stage. CA Foundation syllabus, course papers, and all other related information can be accessed on this link.

This paper is divided into 4 parts-

Paper 1: Principles and Practices of Accounting

Paper 2: Mercantile Law and General English

Paper 3: Business Mathematics, Logical Reasoning, and Statistics

Paper 4: Business Economics & Business and Commercial Knowledge

Stage 2 – IPCC or IPCE

After the results for CA Foundation, the candidates get a period of 9 months to prepare for the next stage, which is the intermediate stage.

The next stage in the CA course is IPCC/IPCE (Integrated Professional Competence Course/Examination). A candidate reaches this stage after clearing CA – Foundation. IPCC is divided into two groups;

Group – 1

Group – 2

For clearing this stage a student needs to get a minimum of 40 marks in each stage and a total of 50% in aggregate in each group. Students need to appear in Intermediate Examination on completion of 8 months of study course as on the first day of the month in which the examination is to be held.

Stage 3 – Apprenticeship training

The next stage for candidates who have cleared both the groups of IPCC/IPCE and even any one of the groups is apprenticeship training of 3 years. Though, before that, one must go through the ITT and Orientation Program.

After the one can go ahead with the practice, it can be done under any practicing CA or a chartered accountancy firm.

A candidate is not eligible to appear in CA – Final exams if he/she has not completed the apprenticeship training of 3 years.

One always prefers to go with firms like Big 4 or various other big firms. The bottom line stays the same, which says the practice is the Key. It is very important to get the most possible exposure during this period, which helps one place better in a dream company later on. We have to trust that there is no substitute for learning.

Stage 4 – CA Final

The last stage of the CA course is CA – final examination. A candidate who has cleared both groups of IPCC/IPCE and who has completed the apprenticeship training is eligible to apply for CA – Final exams. This is the final stage of CA course.

CA – Final is divided into two groups and each group has four papers.

CA Final Group I

Paper 1: Financial Reporting (100 Marks) Paper 2: Strategic Financial Management (100 Marks) Paper 3: Advanced Auditing and Professional Ethics (100 Marks) Paper 4: Corporate Laws and other Economic Laws (100 Marks)

CA Final Group II

Paper 5: Strategic Cost Management and Performance Evaluation (100 Marks) Paper 6: Elective Paper (100 Marks)

For clearing CA – Final a student needs to get at least 40% marks in each paper and a minimum total of 50% in aggregate in each group to clear this stage. After successfully completing the CA Final exam, one can enroll as a member of the ICAI and be designated as “Chartered Accountant”. Which is just like the final step to dream come true.

So you are done with your graduation and now you may be looking forward to a post-graduate masters degree which focuses on accounting, management, commerce etc.

If you’re looking to study regular college then the top regular commerce colleges are the ones you are looking for such as SRCC, Loyola, Xaviers etc. MCOM from IGNOU is a suitable choice for someone who is looking for a distance program. SOMS or School of Management Studies is the department which has the responsibility of the design and delivery of all IGNOU’s management courses.

Details of MCOM from IGNOU

Eligibility

You need to be a graduate from a recognized university

Minimum Duration

2 Years

Maximum Duration

5 Years

Course Fees

Rs 11,000

Age

There is no age bar

Language

Hindi/English

Session Time

July – December & January – June

Others

Expect 6 Subjects each year with 6 Credits each

Other Course Details

Some features of this program are:

Material provided for studies is enriched with multimedia to assist students in their learning and growth.

Operational activities of business are kept in the limelight which helps in a more practical understanding of the real life scenarios.

Teleconferencing is encouraged and has been included as a regular practice.

Students

From IGNOU you can also choose to do MCOM which focuses on specific area of study such as:

MCOM in Finance & Taxation, Click Here for more details on MCOM (F&T)

MCOM in Business Policy & Corporate Governance, Click Here for more details on MCOM (BP&CG)

MCOM in Management Accounting & Financial Strategies, Click Here for more details on MCOM (MA&FS)

After 10+2 you can now head towards graduation which in India is offered by both private and the public sector. Graduation is necessary to apply for a lot of jobs both with private and the public companies. BCOM from IGNOU is suitable for someone who is looking to attain a graduation degree through distance education.

BCOM has been included under SOMS or School of Management Studies, it handles all the management related courses’ design and delivery from IGNOU.

There are many universities which offer bachelors in commerce such as IGNOU, SOL (School of open learning, Delhi University), SMU (Sikkim Manipal University) and many other regional universities from Andhra, Bangalore, Madras, Patna etc.

Details of BCOM from IGNOU

Eligibility

You need to be at least 10+2 qualified or must have completed BPP program from IGNOU

Minimum Duration

3 Years

Maximum Duration

6 Years

Course Fees

Rs 6,000

Age

There is no age bar

Language

Hindi/English

Others

Expect 6 Subjects in 1st year, 13 in 2nd year, 16 in 3rd year

Other Course Details

Some features of this program are:

With BCOM from IGNOU students can also get basic knowledge about Computers, Tech, Humanities, Social Sciences etc.

All the teaching is done through multi media medium which makes the studies interactive for the students.

If you are a student from a different university and want admission in BCOM from IGNOU on the basis of prior education, you can apply.

From IGNOU you can also choose to do BCOM which focuses on specific area of study such as:

BCOM in Accountancy & Finance, Click Here for more details.

BCOM in Corporate Affairs and Administration, Click Here for more details.

BCOM in Financial and Cost Accounting, Click Here for more details.

An Accounting software is used by almost all micro, small & medium firms to make it easier and user-friendly for the owners to manage the finances of a company. It helps provide more accurate results with less efforts. Top accounting softwares in india include Tally, Marg, Busy & Quickbooks.

Not all companies need an ERP package. It depends on the size of the company, amount of money the company is planning to spend on it, user-interface & complexity of the software.

Tally

Tally is a company founded by Shyam Sundar Goenka and is Headquartered in Bangalore, India. (2014) It currently serves over 100 nations worldwide & has a revenue of US$ 90mn. Top 4 countries with a wide use of Tally are India, Bangladesh, Middle East & United Kingdom. It has over 500,000 subscribers in India alone.

The latest update, TallyERP9 is customized to many Indian accounting rules and regulations. It is considered an easy to implement accounting software and people who are well versed with operating Tally are available in large number.

It also has few other products on offer such as Tally: Developer 9, Shopper 9 & Tally.Server 9999

To check pricing and consider buying Tally Click Here

QuickBooks

Quickbooks is the leader of accounting softwares with over 6,00,000 subscribers (2014), it is promoted & developed by an American software company “Intuit”. The company is headquartered in Mountain View, California & is publicly traded on NASDAQ.

Intuit mainly focuses on small businesses and accountants by serving them with financial and tax planning softwares. Quickbooks is widely used in many countries and each country has a different product that would suit the country’s business rules and customs.

It is also offered on the cloud platform with a different name “QBO” and can be installed in the mobile phones too. It is used for invoicing, billing to the customers and day-to-day transactions.

To check pricing and consider buying QuickBooks Click Here

Marg

Marg or Marg Compusoft is a provider of unified business application software for SMEs. Its journey began around 1992 in the field of pharmaceutical informatics and information technologies in general. (2014) It has over 160 sales & support centers, 700 ERP clients & 45000 Satsfied users.

Marg offers financial accounting software which suits companies that do not need a complex ERP package. For almost two decades, many small businesses in India are using this software. This software suits most of the FMCG, pharmaceutical and other companies.

To check pricing and consider buying Marg Click Here

Busy

Busy or Busy Infotech Pvt. Ltd. which is a sister concern of Digitronics Infosolutions Pvt. Ltd. started back in the year 1997. Currently the chairman is Mr. Harish Chander & the managing director is Dinesh Kumar Gupta.

Busy is an accounting software that is used in many industries mainly within Micro and SME segment. Currently it has more than 6,00,000 users across the globe. Busy can support functions ranging from financial accounting, invoicing, Taxes, MIS reports etc.

You can download a 30 days trial copy or purchase a full version Click Here

Companies which are looking for small software unlike an ERP package can opt for many small and effective software packages, instead of spending money unnecessarily on large packages. One needs to choose the software based on the company’s requirement.

Most softwares can be upgraded and can grow and become flexible as the company grows. Look into the features of each software and pick the one that covers most of your requirements.

With the information age hitting us, gone are the days when getting a passport was regarded as a daunting task. Now, you can apply for a passport online and avoid the queue. On a busy day to steer clear of this hassle, you might not bother shedding few notes to the passport agent. However, the changes in the procedure across the nation has eased the process to a greater extent. Now you can apply for a passport online through this website http://passportindia.gov.in.

Following are the steps you need to follow to apply for a passport online:

Fill in all mandatory asterisk (*) marked fields as per the given instructions. Please carefully select the passport office as per your present address only. Once you are done with the entry, click on “Register” and you are done with the registration process.

Check your inbox and look for an email from “[email protected]“, open the email and follow the link in emthe ail to activate your user account.

Click on the ‘Apply for Fresh Passport/Re-issue of Passport’ link on your home screen.

Choice 1 – You can download the soft copy of the form, fill it out offline & upload it.

Choice – 2 – You can fill in all the required details in the online application form under the head Alternative 2 by clicking on the link provided on the page (Please note that an internet connection would be required when you opt for online application).

**Make sure you check your information twice or thrice if needed before submitting a form offline or online.

The next step is to make payment for the application. Click on the ‘View Saved/Submitted Applications’ link on the left side of the screen under the Services screen to schedule an appointment. Then Click on the ‘Pay and Schedule Appointment’ link to make payment to schedule an appointment.

Please note that payments for appointments at all Passport Seva Kendras (PSK) have been mandatorily made Online. The same can be done by any one of the following modes:

Credit/Debit Card (MasterCard and Visa)

Internet Banking (State Bank of India and Associate Banks Only)

SBI Bank Challan

Once you are done with the payment step, Click on the ‘Print Application Receipt’ link to print the application receipt. This application receipt shall be demanded by the PSK. For easy reference place this receipt bearing the Application Reference Number/Appointment Number in front of your passport application file.

Reach the PSK with all the original documents at least 30 minutes before the appointment time to avoid any unnecessary delay. If you are not sure of dthe ocuments that would be required at PSK, click on the below link and follow the given instructions.

Big Four is the term given to represent the top four audit companies of the world. Ernst and Young, Deloitte, PricewaterhouseCoopers and KPMG together make the Big Four. These companies conduct the audit of many public and private companies throughout the world.

They audit more than 80% of all the public companies in the United States and specialize in other areas such as assurance, actuarial, risk management, corporate legal services, tax, financial planning and consulting.

Initially, there were the Big Eight:

Coopers & Lybrand

Ernst & Whinney

Price Waterhouse

Arthur Andersen

Arthur Young & Co.

Touche Ross

Peat Marwick Mitchell

Arthur Young & Co.

1989 June – Ernst & Whinney merged with Arthur Young to form Ernst & Young

1989 Aug – Deloitte, Haskins & Sells merged with Touche Ross to form Deloitte & Touche

1998 July – Price Waterhouse merged with Coopers & Lybrand to form PricewaterhouseCoopers

So the world was left with only the Big Five which included Arthur Anderson. After the infamous scandal of Enron, Arthur Anderson went out of business and Big Five became the now famous Big Four.

Deloitte

Head Quarters – 30 Rockefeller Plaza, New York City, New York, USA

Employees – Over 200,000 (2014)

Revenue – Over US$ 34 Billion (2014)

Countries Served – Over 150 (2014)

Found back in 1845 at London, United Kingdom, Deloitte started as the separate companies of William Deloitte, Charles Haskins, Elijah Sells, and George Touche. The three companies eventually merged to become Deloitte & Touche.

Although acquisitions and mergers did help them to an extent but they have mainly remained on the top with the help of strong dedication and commitment towards their clients. In 2011, Deloitte had 1.8% growth and PWC had 1.5% growth, making Deloitte the top firm among the audit companies. In 2011, PWC out-ranked Deloitte and in 2013, Deloitte again took the first place.

Their estimated annual growth for 2012 was 8%, which is the highest out of the big four accounting firms. They have upheld this growth rate over the past four years.

PricewaterhouseCoopers

Head Quarters – London, United Kingdom

Employees – Over 195,000 (2014)

Revenue – US$ 34.0 Billion (2014)

Countries Served – Over 150 (2014)

Founded back in 1849 by Samuel Lowell Price It is the second largest audit firm operating in approximately 157 countries. It re branded itself to PWC in 1998 when Coopers & Lybrand and Price Waterhouse merged together. Their major revenue source as of 2014 is Assurance, Advisory & Tax practice. Its headquarters are in London, UK.

The firm has sustained its growth over the years, acquiring and merging with other company’s such as Booz & Co., leading them to become one of the biggest firms in the world & 5th largest in the US.

PWC has reached this level with acquiring skill from over 750 offices across the world it is growing at the pace of 4% every year.

Ernst and Young (EY)

Head Quarters – London, United Kingdom

Employees – 190,000 (2014)

Revenue – Over US$ 27 Billion (2014)

Countries Served – Over 150 (2014)

Found back in 1849 by Harding & Pullein in England. It reformed to Ernst & Young in 1989 when Ernst & Whinney and Arthur Young & Co. merged together. With more than 700 offices throughout the world EY is rated third among the top 20 accounting firms in the United States.

Top source of income for EY include Assurance, Tax & Advisory.

In 2013 EY reported revenue of $25.8 billion and 5.8% annual growth rate which is the highest growth rate it has seen over the past 5 years. This is up 1.4% YOY 2012.

KPMG

Head Quarters – Amstelveen, Netherlands

Employees – Over 160,000 (2014)

Revenue – Over US$ 24 Billion (2014)

Countries Served – Over 150 (2014)

History of KPMG can be traced back to 1870. In 1979 KMG was formed which was further joined by Peat Marwick and the name was eventually changed to KPMG in the late early 90s. Not a lot of people would know that in 1997 EY & KPMG tried to merge and the announcement was also made however it couldn’t happen due to some reasons.

Major source of income for KPMG is Audit, Advisory & Tax.

KPMG is doing fairly well with its growth and has also earned a lot of accolades over the years such as world’s most attractive employer, (2nd) World’s best outsourcing advisers etc.

Good to know – 5th largest accounting firm is said to be BDO International with over US$ 7Billion revenues (2014) & number 6 is Grant Thornton with over US$ 4 Billion revenues (2014).

The word contingent or contingency means “possible, but not certain to occur”. Contingent assets are those assets which may or may not become a reality for a business depending on the outcome of a future event. The existence of this kind of asset is completely dependent on the occurrence of a probable event in future. It is a potential asset but there is no surety.

An example of such an asset is a court case. Only if the company wins the court case & gains from it, the contingent asset will actually be realized.

A contingent asset may be disclosed as a footnote to the balance sheet, These are not recognized in financial statements since this may result in recognition of income that may never be realized. Unlike contingent liabilities, contingent assets are not recorded even if they are probable and the amount of gain can be estimated.

The only exception to recording a contingent asset is where an inflow of economic benefits is sure or in other words virtually certain such as a settled lawsuit (where the benefit is sure to be received) may be disclosed & recorded in the period when the change actually occurs.

Example

Let us suppose that Unreal Pvt Ltd. files a case of patent violation on Real Pvt. Ltd. Now, the former can’t recognize this as a contingent asset even if it is sure to win and the amount can be estimated. Only when the lawsuit is settled and a sure amount is to be received at a specific time can this be recognized in the books of Unreal Pvt Ltd. as a Contingent Asset.

Short Quiz for Self-Evaluation

Loading

Your quiz has been submitted

Want to re-attempt? - “Refresh” this page.

Check out more content on our site :)

Subscribed? - Check your mailbox

Thank You!

Server Side Error

We faced problems while connecting to the server or receiving data from the server. Please wait for a few seconds and try again.

If the problem persists, then check your internet connectivity. If all other sites open fine, then please contact the administrator of this website with the following information.

Nowadays, businesses sell their assets as part of strategic decision-making. Reasons could vary from up-gradation to new better quality asset, arranging money for a business need, not in use asset etc. there could be any reason to sell an asset.

It is common that an asset may not be sold at its current book value if it is sold for more, it generates profit for the business and, in the situation opposite to that, it incurs a loss when it is sold for less.

Journal entry for loss on sale of fixed assets is shown on the debit side of profit and loss account.

There are 3 different accounts that will be affected by this

The asset being sold

The cash being received

A loss incurred on the sale of an asset

Journal Entry for Loss on Sale of Fixed Assets

Cash A/C

Debit

Real Account

Debit what comes in

Loss on sale of asset

Debit

Nominal Account

Debit all losses

To Sale of Asset

Credit

Real Account

Credit what goes out

Short Quiz for Self-Evaluation

Loading

Your quiz has been submitted

Want to re-attempt? - Simply “refresh” this page.

Please check out more content on our site :)

Subscribed? - Check your mailbox

Thank You!

Server Side Error

We faced problems while connecting to the server or receiving data from the server. Please wait for a few seconds and try again.

If the problem persists, then check your internet connectivity. If all other sites open fine, then please contact the administrator of this website with the following information.

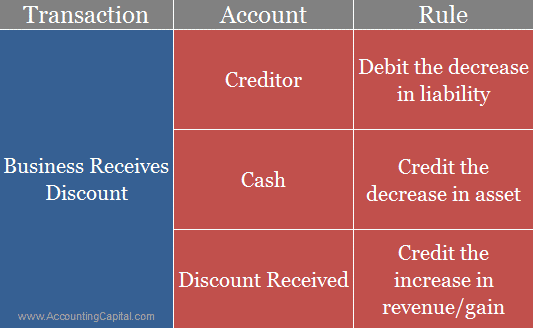

Discounts are common in both B2B and B2C transactions to push both credit and cash sales, they are usually given in lieu of some consideration which can be prompt payments, trade practices, recoveries, etc. While posting a journal entry for discount received “Discount Received Account” is credited.

Discount received acts as a gain for the business and is shown on the credit side of a profit and loss account. Trade discount is not shown in the main financial statements, however cash discount and other types of discounts are shown in books of accounts.

Journal entry for discount received is essentially booked with the help of a compound journal entry.

Discount received by a buyer is discount allowed in the books of the seller. Following examples explain the use of journal entry for discount received in the real-world scenarios.

Examples – Accounting for Discount Received

Payment made to Unreal Co. in cash for goods purchased worth 5,000 at 10% discount. (Discount received in the regular course of business)

Unreal Co. A/C

5,000

To Cash A/C

4,500

To Discount Received A/C

5,00

Paid 2,000 to Unreal Co. in cash for full and final settlement of their account worth 10,000. (Discount received to settle an overdue payment)

Unreal Co. A/C

10,000

To Cash A/C

2,000

To Discount Received

8,000

Short Quiz for Self-Evaluation

Loading

Your quiz has been submitted

Want to re-attempt? – “Refresh” this page.

Check out more content on our site :)

Subscribed? – Check your mailbox

Thank You!

Server Side Error

We faced problems while connecting to the server or receiving data from the server. Please wait for a few seconds and try again.

If the problem persists, then check your internet connectivity. If all other sites open fine, then please contact the administrator of this website with the following information.

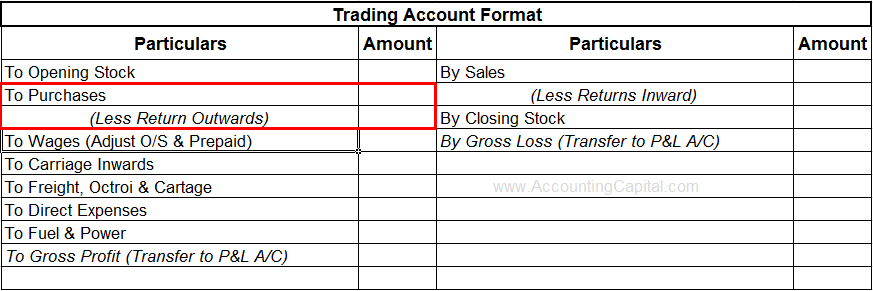

Return outwards are goods returned by a customer to the seller. They are goods that were once purchased from external parties, however, because of being unsatisfactory they were returned back to them, they are also called Purchase returns.

Outward returns reduce the total accounts payable for a business. It is a sales return and on the other, it is a purchase return. The transaction in both cases is reversed and the related sale or purchase is nullified.

Purchase returns reduce the total purchases/accounts payable of a company and the deduction is shown in the trading account. A subsidiary book called Purchase returns book is prepared to record all such entries.

Journal Entry for Return Outwards

Supplier’s A/C

Debit

Debit the decrease in liability

To Return Outwards A/C

Credit

Credit the decrease in expense

Supplier – This is a reduction in payables for the business.

Return Outwards – This is a reduction in expenses for the business.

Shown in Trading Account (Deducted from Purchases)

Let’s suppose that a company “Unreal Pvt Ltd.” returned goods worth 10,000 to its supplier “Star Pvt Ltd.”. The journal entry to record these returns in the books of Unreal Pvt Ltd. will be as follows;

Star Pvt Ltd. A/C

10,000

To Return Outwards A/C

10,000

Reasons for Purchase Returns

An incorrect product or size was ordered by the customer. (customer’s mistake)

An incorrect product or size was sent by the seller. (seller’s mistake)

Damaged or defective products received. (product damaged)

The quality of the product was not as expected. (bad quality)

Late delivery of the product. (timing)

The buyer purchased an excessive amount. (quantity)

Better price found by the buyer with another seller. (price options)

Short Quiz for Self-Evaluation

Loading

Your quiz has been submitted

Want to re-attempt? - “Refresh” this page.

Check out more content on our site :)

Subscribed? - Check your mailbox

Thank You!

Server Side Error

We faced problems while connecting to the server or receiving data from the server. Please wait for a few seconds and try again.

If the problem persists, then check your internet connectivity. If all other sites open fine, then please contact the administrator of this website with the following information.

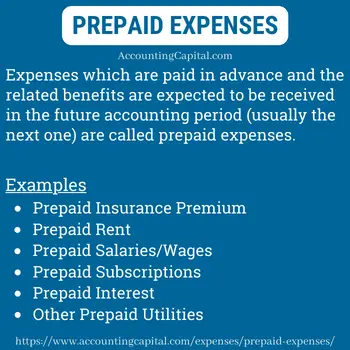

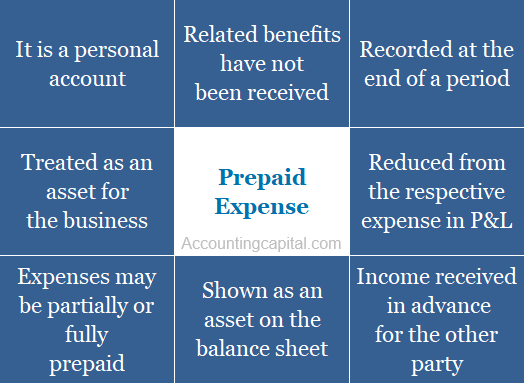

Prepaid expenses are those expenses which have been paid in advance and the related benefits are not received within the same accounting period. The benefits of expenses incurred are carried forward to the next accounting period. Prepaid expenses are treated as an asset by the business.

Examples – Prepaid salary, prepaid rent, prepaid subscription, etc. They are recorded in books of finance at the end of an accounting period to show the true numbers of a business. They are also known as unexpired expenses or expenses paid in advance.

Examples

Company-A has a rent obligation of 80,000/year that is due every time on the 10th of Jan, this year the company decides to pay double that is full rent in advance for next year.

The amount paid in advance for next year is 80,000 which is prepaid and termed as a “prepaid expense” for Company A.

At the end of the period, this “amount paid in advance” impacts the financials of the business. Such a transaction is supposed to be journalized.

According to the accrual concept of accounting, transactions are recorded in the books of accounts at the time of their occurrence and not when the actual cash or a cash equivalent is received or paid.

Based on the above principle, payments are not necessarily made immediately they may be late or in advance. Outstanding expenses and unexpired expenses are both a result of this.

Advance payment made for an expense has two steps for being recorded and recognised. Firstly, when the prepayment is done and secondly when the related expense becomes due.

a) At the time of advance payment of the expense.

Prepaid Expense A/c

Debit

Debit the increase in asset

To Bank A/c

Credit

Credit the decrease in asset

(Being expense paid in advance for the period)

b) At the time when the expense becomes due to be paid.

Expense A/c

Debit

Debit the increase in expense

To Prepaid Expense A/c

Credit

Credit the decrease in asset

(Adjustment entry made to recognize the expense on the due date)

Alternate Scenario

In some cases, expenses are prepaid along with the actual payment made on the due date. In such a case, when the date is the same then a compound journal entry can also be recorded.

Expense A/c

Debit

Debit the increase in expense

Prepaid Expense A/c

Debit

Debit the increase in asset

To Bank A/c

Credit

Credit the decrease in asset

(Being expense paid along with prepaid expense paid in advance for a future period)

Prepaid Expenses in Trial Balance

If prepaid expense already appears inside the trial balance then it implies that the adjusting entry has already been posted.

In this case, it is only shown on the balance sheet as a “current asset” and no adjustment is required in the income statement.

In the event that such an expense does not appear in the trial balance, they should be added to the respective accounts. This should be reflected on the debit side of the Profit and Loss Account.

An insurance premium is an amount paid to cover the cost of coverage associated with an insurance agreement. It is often paid monthly, quarterly, half-yearly, or yearly.

When an insurance premium has been paid to the insurance company but the related coverage hasn’t yet begun, this is known as insurance premium prepaid.

Prepaid insurance journal entry should be recorded as follows:

a) At the time insurance premium is prepaid.

Prepaid Insurance Premium A/c

Debit

To Bank A/c

Credit

(Being insurance premium paid in advance)

b) On the date the prepaid insurance premium becomes due.

Insurance Expense A/c

Debit

To Prepaid Insurance Premium A/c

Credit

(Insurance expense being recognized and the related prepaid asset being reduced)

When the insurance premium is due, the amount due is deducted from the prepaid account and is shown as an operating expense in the Profit and Loss A/c prepared for the current period.

The term “rent” refers to a periodic payment that covers the expenses associated with occupying and using a property (such as land, buildings, etc.) The payments are made to the owner of the property. Usually, it is paid on a monthly or annual basis.

The term “outstanding rent” refers to rent due for a period that has already passed.

Prepaid rent journal entry should be recorded as follows:

a) At the time rent is paid in advance.

Prepaid Rent A/c

Debit

To Bank A/c

Credit

(Being rent paid in advance)

b) On the date the prepaid rent becomes due.

Rent Expense A/c

Debit

To Prepaid Rent A/c

Credit

(Rent expense being recognised and the related prepaid asset being reduced)

On the date when rent expense is actually due, the amount is deducted from the prepaid rent account and is shown as an operating expense in the Profit and Loss A/c prepared for the current period.

In exchange for the work that an employee performs, an employer pays them a salary. It is often paid monthly and accompanied by some benefits.

When a salary is paid in advance to an employee but the employee is yet to work for that period it is called salary paid in advance.

Prepaid salary journal entry should be recorded as follows:

a) At the time salary is prepaid.

Prepaid Salaries A/c

Debit

To Bank A/c

Credit

(Being salary paid in advance)

b) On the date the salary becomes due.

Salaries A/c

Debit

To Prepaid Salaries A/c

Credit

(Salary expense being recognized and the related asset being reduced)

When the actual salary is due, the amount is deducted from the prepaid salaries account and is shown as an operating expense in the current period’s Income Statement.

Assets are resources that belong to a person or entity. They may be tangible or intangible items used to generate economic value for business operations. An expense that is paid before it is due is considered prepaid and it is treated as an asset (current) for the business.

Reason – The logic of why advance payment made for an expense is treated as an asset by the business is because the benefit in exchange for the payment is postponed to a future date. It stays an asset till the time the actual expense is due and recognized accordingly.

Such an expense has an unexpired value which means the benefit in exchange for the payment is still to be received. As a result, it is also called unexpired expense or unexpired cost.

Consider it a slow-burning asset that gradually becomes an expense and exhausts when the actual due date comes around.

Why is it considered a current asset?

Assets that are generally expected to be used, sold, or depleted within the current accounting year (usually 12 months) are called current assets.

The expectation around a prepaid expense is to convert it from being an asset to realising it as an income within a year.

Commonly a business expects to use, sell, or exhaust the current asset within the current accounting period therefore it is regarded as a current asset. In this way, they contribute to the calculation of the current ratio but they are excluded from the list of liquid assets.

In continuation of the previous heading, it is important to know that the prepaid expense is also shown as a reduction from the related direct or indirect expense in the Trading and P&L A/c.

Prepaid Expense is Which Type of Account?

As per the traditional classification of accounts, a prepaid expense is a type of personal account (representative personal). These types of accounts represent a person or a group.

It makes sense to call it a representative personal account since it’s indirectly linked to a person or group. As per the rules of debit and credit, it follows the rule of Dr. the receiver and Cr. the giver.

However, as per modern accounting rules, it is an asset and follows the rule of Dr. the increase and Cr. the decrease.

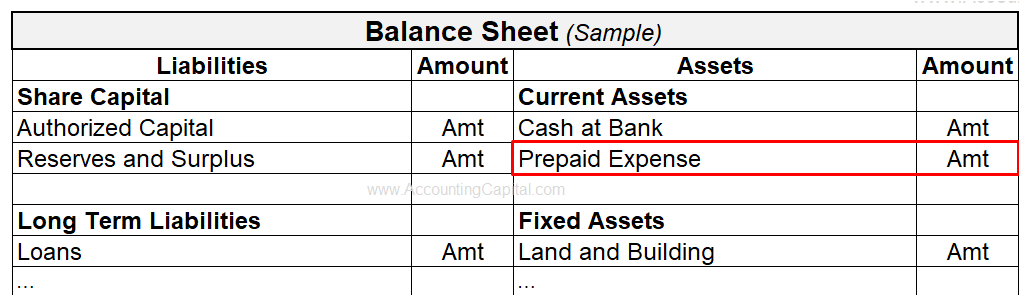

Treatment in Final Accounts

Treatment of Prepaid Expenses in Financial Statements/Final Accounts

Trading & Profit and Loss A/c Show on the Dr. side (subtract from the respective direct or indirect expense)

Balance Sheet: Show on the “Assets” side (under the head “Current Assets”)

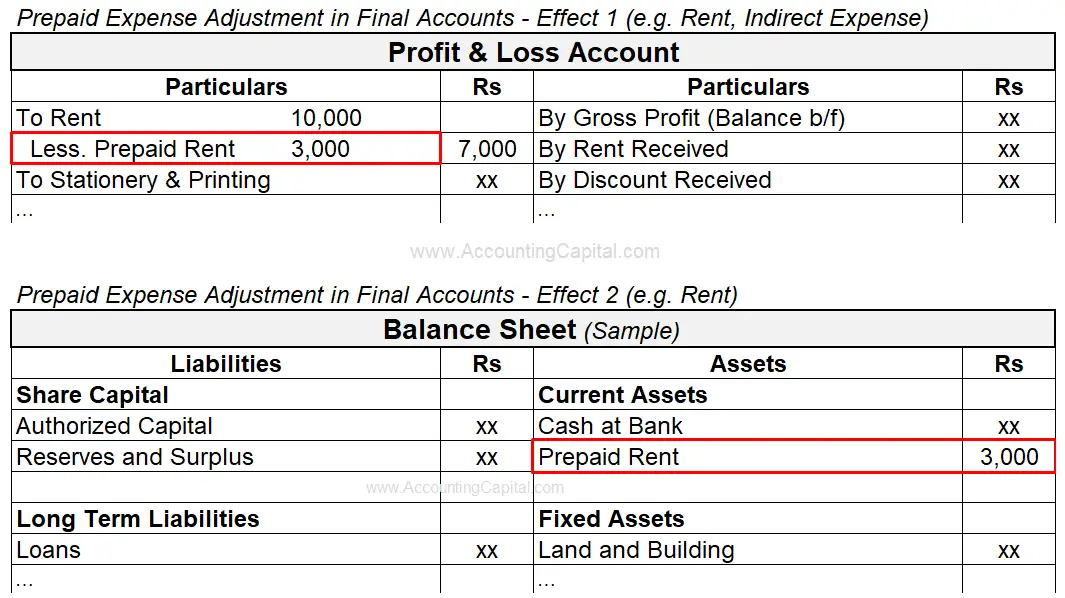

Example

In the year, a company paid Rs 10,000 in rent and estimated the prepaid rent to be Rs 3,000. Adjust prepaid expenses in final accounts at the end of the period.

Revision and Highlights

Highly Recommended!!

Do not miss our 1-minute revision video and the quiz below. This will help you quickly revise and memorize the topic forever. Try them :)

Short Quiz for Self-Evaluation

Loading

Your quiz has been submitted

Want to re-attempt? - Simply “refresh” this page.

Please check out more content on our site :)

Subscribed? - Check your mailbox

Thank You!

Server Side Error

We faced problems while connecting to the server or receiving data from the server. Please wait for a few seconds and try again.

If the problem persists, then check your internet connectivity. If all other sites open fine, then please contact the administrator of this website with the following information.

TextStatus: undefined HTTP Error: undefined

Processing you request

Error

Some error has occured.

Conclusion

Prepaid expenses are also referred to as deferrals, prepayments, deferred expenses, unexpired costs, prepaids, or prepaid liabilities. Some more common examples not shared above are interest expenses, estimated taxes, some utility bills,

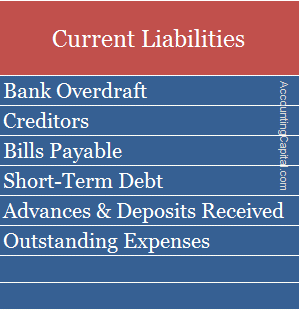

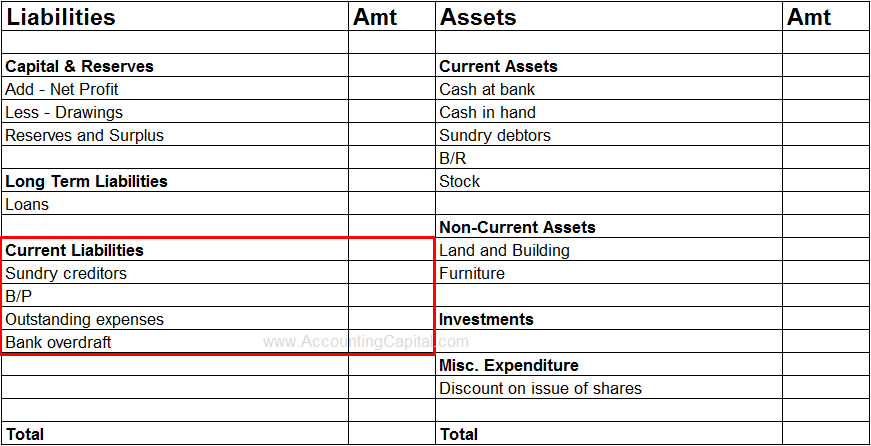

Obligations of a company which are payable within a year or an accounting cycle of a business are called current liabilities. They are either settled by current assets or by the introduction of new short-term liabilities.

Examples include Overdraft, Creditors, Short-term loans, Outstanding Expenses, etc. They are shown on the Liabilities side of the balance sheet.

They play a vital role in the control of the working capital of a business, WC = CA – CL, therefore, more of such short-term obligations mean less working capital and vice-versa.

It is also the denominator when looking at a company’s current ratio thus playing an important part in its liquidity. It is imperative to keep a check on such short-term liabilities.

Current Liabilities in Financial Statements

They are shown in the liabilities section of the balance sheet.

Short Quiz for Self-Evaluation

Loading

Your quiz has been submitted

Want to re-attempt? - Simply “refresh” this page.

Please check out more content on our site :)

Subscribed? - Check your mailbox

Thank You!

Server Side Error

We faced problems while connecting to the server or receiving data from the server. Please wait for a few seconds and try again.

If the problem persists, then check your internet connectivity. If all other sites open fine, then please contact the administrator of this website with the following information.

In the business world, a lot of sales transactions happen on credit, i.e. after a specified period of time. In this scenario, there are two main types of discounts allowed to customers. One is trade discount and the other is a cash discount.

Now, after anticipating the amount of cash discount allowable to debtors, a separate “provision for discount on debtors account” is opened and it is very similar to the “provision for doubtful debts account”. The only difference between the two is that provision for a discount is calculated on the debtors’ balance after deducting the provision for doubtful debts.

Journal Entry to Create Provision for Discount on Debtors

Profit & Loss A/C

Debit

To Provision for Discount on Debtors A/C

Credit

If a provision for discount on debtors exists at the time of providing the discount, then write off the discount from that provision.