A Cash Book is a type of subsidiary book where cash (or) bank receipts and cash (or) bank payments made during a period are recorded in a chronological order. Receipts are recorded on the debit – the left hand side, and payments are recorded on the credit – right hand side.

Entries are recorded just like a ledger account with the help of “To” and “By“. The number of cash transactions in a business is generally large, hence it is convenient to have a separate cash book to record such transactions.

In case a transaction affects both the cash and the bank account, a contra entry is recorded. There are 3 types of a cash book.

Single Column Cash Book

Also known as a simple cash book or a one column cash book, a single column cash book has one relevant column on each side which shows the simple “receipts” and “payments” of cash. Receipts are shown on the left side and the right side is for payments.

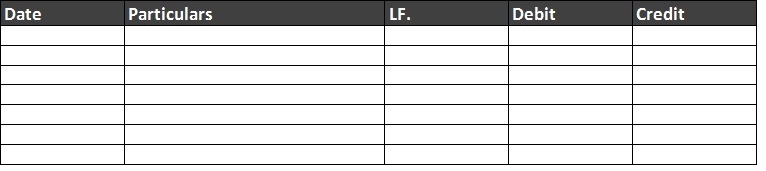

Sample Format of One Column Cash Book

Date

Particulars

LF.

Cash

Date

Particulars

LF.

Cash

Receipt Side

Receipt Side

Receipt Side

Receipt Side

Payment Side

Payment Side

Payment Side

Payment Side

Receipt Side

Receipt Side

Receipt Side

Receipt Side

Payment Side

Payment Side

Payment Side

Payment Side

Balancing

Just like any other account, it is balanced at the end of a period. The total of receipts should always be greater than the payments. The difference is mentioned on the credit side as “Balance c/d”. The balance on the debit side is then written with “To Balance b/d”, this is the beginning cash balance of a business for the next period.

Double Column Cash Book

Also known as a two column cash book, a double column cash book is the one which has a “Bank” column in addition to the regular “Cash” column. Just like the other type of books, it records receipts from cash and bank on the left side and payments – on the right side.

Sample Format of Two Column Cash Book

Date

Particulars

Cash

Bank

Date

Particulars

Cash

Bank

Triple Column Cash Book

Also called a three column cash book, a triple column cash book has “Cash”, “Bank” and “Discount Allowed” on the receipt on the left side and “Cash”, “Bank”and“Discount Received” on the payments are on the right side of the cash book. Cash discount is recorded, when payments are made in cash or by check.

Sample Format of Three Column Cash Book

Date

Particulars

Discount

Cash

Bank

Date

Particulars

Discount

Cash

Bank

Short Quiz for Self-Evaluation

Loading

Your quiz has been submitted

Want to re-attempt? - “Refresh” this page.

Check out more content on our site :)

Subscribed? - Check your mailbox

Thank You!

Server Side Error

We faced problems while connecting to the server or receiving data from the server. Please wait for a few seconds and try again.

If the problem persists, then check your internet connectivity. If all other sites open fine, then please contact the administrator of this website with the following information.

Also known as a B/P book, bills payable book is a subsidiary or secondary book of accounting where all bills of exchange, which are payable by the business, are recorded. The total value of all the bills payable for an accounting period is transferred to the books of accounts.

In a mid to large sized business where the number of bills exchanging hands is large in number, it is tough to journalize all bills drawn. All such bills are entered in an accounting ERP or a register depending on the business, furthermore, all these entries are transferred to the respective ledger accounts at a regular interval, often monthly.

A bill receivable for a “drawer” is a bill payable for a “drawee”. Bills payable account will usually have a credit balance, as it is supposed to be paid at maturity, it acts as a liability for the business. Generally, every bill has a 3-day grace period.

Sample Format of a B/P Book

The person, who draws the bill of exchange, is called a “drawer” and the customer, on whom it is drawn, is called a “drawee” or an “acceptor”.

Short Quiz for Self-Evaluation

Loading

Your quiz has been submitted

Want to re-attempt? - “Refresh” this page.

Check out more content on our site :)

Subscribed? - Check your mailbox

Thank You!

Server Side Error

We faced problems while connecting to the server or receiving data from the server. Please wait for a few seconds and try again.

If the problem persists, then check your internet connectivity. If all other sites open fine, then please contact the administrator of this website with the following information.

Also known as a B/R book, bills receivable book is a subsidiary or secondary book of accounting, where all bills of exchange, which are receivable for the business, are recorded. The total value of all the bills receivable for an accounting period is transferred to the books of accounts.

In a mid to large sized business where the number of bills exchanging hands is large in number, it is tough to journalize all receipt of bills. All the bills are entered in an accounting ERP or a register depending on the business, furthermore, all these entries are transferred to the respective ledger accounts at a regular interval.

Bills receivable account will usually have a debit balance. As a bill receivable is supposed to be received at maturity, it acts as a current asset for the business. Generally, every bill has a 3 day grace period.

Sample Format of the B/R Book

A person who draws the bill of exchange is called a “drawer” and a customer on whom it is drawn is called a “drawee” or an “acceptor”. A bill receivable for a “drawer” is a bill payable for a “drawee”.

Short Quiz for Self-Evaluation

Loading

Your quiz has been submitted

Want to re-attempt? - “Refresh” this page.

Check out more content on our site :)

Subscribed? - Check your mailbox

Thank You!

Server Side Error

We faced problems while connecting to the server or receiving data from the server. Please wait for a few seconds and try again.

If the problem persists, then check your internet connectivity. If all other sites open fine, then please contact the administrator of this website with the following information.

Journal Proper is mainly used for original records of a transaction which due to their importance or rareness of occurrence do not find a place in any of the subsidiary books of accounting. It is also known as a Miscellaneous Journal and it looks much like any other journal.

Sample Format of a Journal Proper

Types of entries that are entered in the journal proper:

As the name suggests, opening entries are recorded at the beginning of a financial period. The balances mentioned in the balance sheet of the previous year are brought forward by recording the liabilities, capital, and assets from the previous year.

Example

The rule to be applied to make an opening entry is

Assets A/C

Debit

To Liabilities A/C

Credit

To Capital A/C

Credit

Sample Format of an Opening Entry in a Journal Proper

Date

Particulars

LF.

Debit

Credit

mm/dd

Cash A/C

35,000

Furniture A/C

15,000

To Sundry Creditors A/C

24,000

To Capital A/C

26,000

All amounts mentioned in the sample format are the closing balances of the previous year balance sheet.

Closing Entries

Almost the opposite of the opening entries, they are recorded at the end of a financial period; closing entries are related to nominal accounts. These accounts are closed by transferring their balances to trading and profit and loss accounts. A record is not included in the ledger without a journal entry, so closing entries are recorded with the help of a journal proper and then recorded in the ledger.

Example

Profit & Loss A/C

Debit

To Salaries A/C

Credit

At the end of a period Salary account is closed by transferring its balance to profit and loss account.

Rectification Entries

In the world of accounting erasing or removing a journal entry once recorded is a strict NO!. Mistakes should only be corrected by passing another entry in the journal.

Example

Purchase for 10,000 was omitted by mistake, it belonged to Unreal Pvt Ltd.

Rectification entry, in this case, will be

Purchase A/C

10,000

To Unreal Pvt Ltd.

10,000

Transfer Entries

In simple terms, the transfer entry is used to transfer an item from one account into another. All such transfers are made with the help of journal entries.

Example

Let us take an example where a general reserve is created for a business by transferring 5,00,000 from the profits.

Date

Particulars

LF.

Debit

Credit

mm/dd

Profit & Loss A/C

5,00,000

To General Reserve

5,00,000

Adjustment Entries

The amount of expenses or incomes may need to be adjusted for advances paid or received at the end of a financial period, these types of adjustments are made with the help of a journal entry. They are very common at the end of an accounting period. Adjustment entries are mainly used for accrual or depreciation related entries.

Example

There are outstanding wages of 50,000 which need to be accounted for

Date

Particulars

LF.

Debit

Credit

mm/dd

Wages A/C

50,000

To Outstanding Wages A/C

50,000

Miscellaneous or Other Entries

In addition to the above entries, there are other entries that can be recorded in a journal proper. They are:

Discount allowed and received

Purchase or sale of items on credit other than goods

Effects of accidents such as losses due to fire

Consignment and joint venture transactions

Endorsement and dishonour of bills of exchange

Transaction for goods distributed as samples

Sale of obsolete assets

Short Quiz for Self-Evaluation

Loading

Your quiz has been submitted

Want to re-attempt? - “Refresh” this page.

Check out more content on our site :)

Subscribed? - Check your mailbox

Thank You!

Server Side Error

We faced problems while connecting to the server or receiving data from the server. Please wait for a few seconds and try again.

If the problem persists, then check your internet connectivity. If all other sites open fine, then please contact the administrator of this website with the following information.

When a business sends the ordered goods back to a vendor it is recorded in the sales return book. At times the buyer may return goods due to poor quality, inaccurate quantity, untimely delivery or other reasons. It is also called returns inwards and an appropriate sales return or a returns inward book is maintained.

All returns are primarily recorded in the sales return book unless the returns are not that frequent, in which case they are recorded in the journal.

Sample Format of Sales Return Book

Date

Particulars

Credit Note No.

LF.

Currency

Amount

Note: A column for “Remarks” can also be added to the Sales return book which would include a brief description of the reason why the goods were returned.

When the goods are returned by the customer, a credit note will be prepared and sent out to his name. A duplicate copy is kept for recording and reference purposes. The returns inward book is totalled at the end of each month.

How to Post Entries from Sales Return Book into Ledger?

After the sales return book is properly updated and all transactions are entered into it, the total of the items is transferred to the ledger in an account called the “Sales returns account”

At the end of the day, each entry is posted to the credit side of the appropriate individual’s account in the Debtors’ledger as this helps the account to remain up to date.

At the end of the month, the total of the “Amount” column is posted to the general ledger with the help of following journal entry.

Let’s assume that total sales returns made at the end of a month are 50,000.

Returns made by A are 30,000.

Returns made by B are 20,000.

These 4 different ledger accounts will be updated from the sales returns book.

Sales Return A/C

Date

Particulars

Amt

Date

Particulars

Amt

mm/dd

To Sundry Debtors A/C

50,000

Sundry Debtors A/C

Date

Particulars

Amt

Date

Particulars

Amt

mm/dd

By Sales Returns A/C

50,000

A’s Account

Date

Particulars

Amt

Date

Particulars

Amt

mm/dd

By Sales Returns A/C

30,000

B’s Account

Date

Particulars

Amt

Date

Particulars

Amt

mm/dd

By Sales Returns A/C

20,000

Short Quiz for Self-Evaluation

Loading

Your quiz has been submitted

Want to re-attempt? - “Refresh” this page.

Check out more content on our site :)

Subscribed? - Check your mailbox

Thank You!

Server Side Error

We faced problems while connecting to the server or receiving data from the server. Please wait for a few seconds and try again.

If the problem persists, then check your internet connectivity. If all other sites open fine, then please contact the administrator of this website with the following information.

At times it may be necessary to return few goods back to a supplier when an order is received, this may be due to poor quality, inaccurate quantity, untimely delivery or other reasons. Purchase returns are also called returns outward and an appropriate purchase returns/returns outward book is maintained.

All returns are primarily recorded in the purchase returns book unless the returns are not that frequent, in which case they are recorded in the journal.

Sample Format of Purchase Returns Book

Date

Particulars

Debit Note No.

LF.

Details

Amount

Note: A column for “Remarks” can also be added to the purchase book which would include a brief description of the reason for why the goods were returned.

When the goods are returned, a debit note will be sent along with them and a debit note number is mentioned in the purchase returns book. In return, the supplier is expected to send a credit note. The returns outward book is totalled at the end of each month.

How to Post Entries from Purchase Returns Book into Ledger?

After the purchase returns book is properly updated and all transactions are entered into it, the total of the items is transferred to the ledger in an account called the “Purchase returns account”.

At the end of the day, each entry is posted to the debit side of the appropriate individual’s account in the creditor’s ledger as this helps the account to stay up to date.

At the end of the month, the total of the “Amount” column is posted to the general ledger with the help of the below-mentioned journal entry.

Journal entry for purchase returns

Creditor A/C

Debit

To Purchase Returns A/C

Credit

Example:Let’s assume that the total purchase returns made at the end of a month are for 50,000.

Returns made to A are 30,000.

Returns made to B are 20,000.

These 4 different ledger accounts will be updated from the purchase returns book.

Purchase Returns A/C

Date

Particulars

Amt

Date

Particulars

Amt

mm/dd

By Sundry Creditors A/C

50,000

Sundry Creditors

Date

Particulars

Amt

Date

Particulars

Amt

mm/dd

To Purchase Returns

50,000

A’s Account

Date

Particulars

Amt

Date

Particulars

Amt

mm/dd

To Purchase Returns

30,000

B’s Account

Date

Particulars

Amt

Date

Particulars

Amt

mm/dd

To Purchase Returns

20,000

Short Quiz for Self-Evaluation

Loading

Your quiz has been submitted

Want to re-attempt? - “Refresh” this page.

Check out more content on our site :)

Subscribed? - Check your mailbox

Thank You!

Server Side Error

We faced problems while connecting to the server or receiving data from the server. Please wait for a few seconds and try again.

If the problem persists, then check your internet connectivity. If all other sites open fine, then please contact the administrator of this website with the following information.

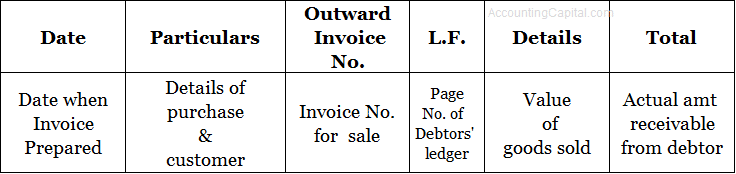

Sales book records all credit sales made by a business. It is one of the secondary book of accounts and unlike cash sales which are recorded in cash book, sales book is only to record credit sales. The amount entered in the sales book is on behalf of invoices supplied to purchasers, however, a copy remains with the firm.

Sales book is also called a Sales Journal or Sales Day Book.

After all the transactions are posted in sales book the business needs to post them to the related ledger accounts. Following are the steps that need to be followed to post the amounts from sales book to the ledger,

Each entry is posted to the debit side of appropriate individual account in the debtor’s ledger at the end of the day, this keeps the accounts up to date.

The column for “Total” is then summed at the end of each month & posted to the ledger.

Journal Entry for Credit Sale

Debtor’s A/C

Debit

To Sales A/C

Credit

Example

Let’s say total sundry debtors at the end of a month are 50,000 where credit sales made from A is 30,000 & B is 20,000 during the period.

Here are the 4 ledger entries that will be recorded,

Sales Account

Date

Particulars

Currency

Date

Particulars

Currency

mm/dd

By Sundry Debtors per Sales Book

50,000

Sundry Debtors Account

Date

Particulars

Currency

Date

Particulars

Currency

mm/dd

To Sales A/C

50,000

A’s Account

Date

Particulars

Currency

Date

Particulars

Currency

mm/dd

To Sales A/C

30,000

B’s Account

Date

Particulars

Currency

Date

Particulars

Currency

mm/dd

To Sales A/C

20,000

Short Quiz for Self-Evaluation

Loading

Your quiz has been submitted

Want to re-attempt? - “Refresh” this page.

Check out more content on our site :)

Subscribed? - Check your mailbox

Thank You!

Server Side Error

We faced problems while connecting to the server or receiving data from the server. Please wait for a few seconds and try again.

If the problem persists, then check your internet connectivity. If all other sites open fine, then please contact the administrator of this website with the following information.

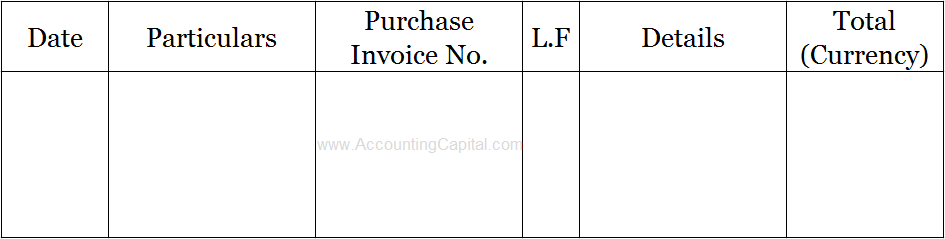

It is also known as a Purchase journal, Invoice book or Purchase daybook. A purchase book is a special-purpose subsidiary book prepared by a business to record all credit purchases. Nowadays all these recordings occur in ERPs and only small firms resort solely to notebooks or MS Excel.

A few things to note are,

Purchases recorded are only for goods or items related to core business operations of a company i.e. goods procured for resale.

Example – If a grocery business purchases office furniture it will not be posted in the purchases book as it is considered as a “purchase of an asset” and not goods.

Cash purchases are recorded in the cash book and credit purchases are recorded in the purchase book.

A reduction granted by a supplier of goods/services on list or catalogue price is called a trade discount. This is done due to business consideration such as trade practices, large quantity orders, etc.

It is not separately shown in the books of accounts; entries recorded in purchase book or sales bookare recorded as the net amount, i.e. Gross Amount – Trade Discount.

It is mainly provided to increase the volume of sales attained by a supplier. It is also known as a functional discount.

Example

Let’s assume that 100 keyboards are sold for the list price of 300 each with a trade discount of 10%.

100 Keyboards X 300 each

30,000

Less 10% of 30,000

30,000 – 3000 = 27,000 (Net Amt)

It is not shown separately instead Net amount is used in the financials.

It is generally recorded in the purchases or sales book, but it is not entered into ledger accounts and there is no separate journal entry. However, here is an example demonstrating how a purchase is accounted in case of trade discount.

Let’s assume that 10 tables are purchased from Unreal Pvt Ltd. at the list price of 3000 per item and 10% discount (trade) is allowed. Accounting for the transaction will happen as follows:

Total list price = 10 x 3000 = 30,000

Less (T.D) = 10% of 30,000 = 3000

Amount to be recorded = list price – discount = 30,000 – 3000 = 27,000

Purchase A/C

27,000

To Unreal Pvt Ltd.

27,000

Short Quiz for Self-Evaluation

Loading

Your quiz has been submitted

Want to re-attempt? - “Refresh” this page.

Check out more content on our site :)

Subscribed? - Check your mailbox

Thank You!

Server Side Error

We faced problems while connecting to the server or receiving data from the server. Please wait for a few seconds and try again.

If the problem persists, then check your internet connectivity. If all other sites open fine, then please contact the administrator of this website with the following information.

A cash discount is a deduction allowed by the supplier of goods or by the provider of services to the buyer from the invoice price. This is done as an incentive in return for paying a bill within a specified time.

Usually, the supplier will reduce the amount owed by a small percentage, e.g. 2%. It can be used by a business to improve the Days Sales Outstanding (DSO). It is not necessary for the supplier to offer a cash discount.

It is shown as an expense in the income statement (profit and loss account)

Few Benefits of Cash Discount

A cash discount is beneficial to the supplier as it allows him to have access to cash much sooner and therefore ensure liquidity to the business.

If used efficiently, a cash discount is beneficial to the buyer as not a mere tool to save some money, but also as a means of maintaining a healthy credit line and a good relationship with the supplier.

Common terms are 2/10, Net 30 (or) 2%/10 days, Net 30. This payment term means that the buyer has an option to avail a 2% cash discount from the invoice price if the payment is made within the first 10 days of receiving the invoice.

If the cash discount is not availed, the net amount due is to be paid within Net 30 days. The payment terms can be modified depending on the supplier’s needs.

Let’s say that 100 keyboards are sold for the invoice price of 300 each and the payment terms are 1/10, Net 30 days.

It means that the buyer will get a 1% cash benefit from the total invoice price if the payment is made within the first 10 days of receipt of the invoice. (Assuming there is no trade discount)

Amount due as per Invoice

30,000

Less Cash Discount 1%

300

Cash to be paid within 10 days

29,700

The buyer has a choice to not avail the discount. In this case, the total amount due will be 30,000 which can be paid within 30 days.

Short Quiz for Self-Evaluation

Loading

Your quiz has been submitted

Want to re-attempt? - “Refresh” this page.

Check out more content on our site :)

Subscribed? - Check your mailbox

Thank You!

Server Side Error

We faced problems while connecting to the server or receiving data from the server. Please wait for a few seconds and try again.

If the problem persists, then check your internet connectivity. If all other sites open fine, then please contact the administrator of this website with the following information.

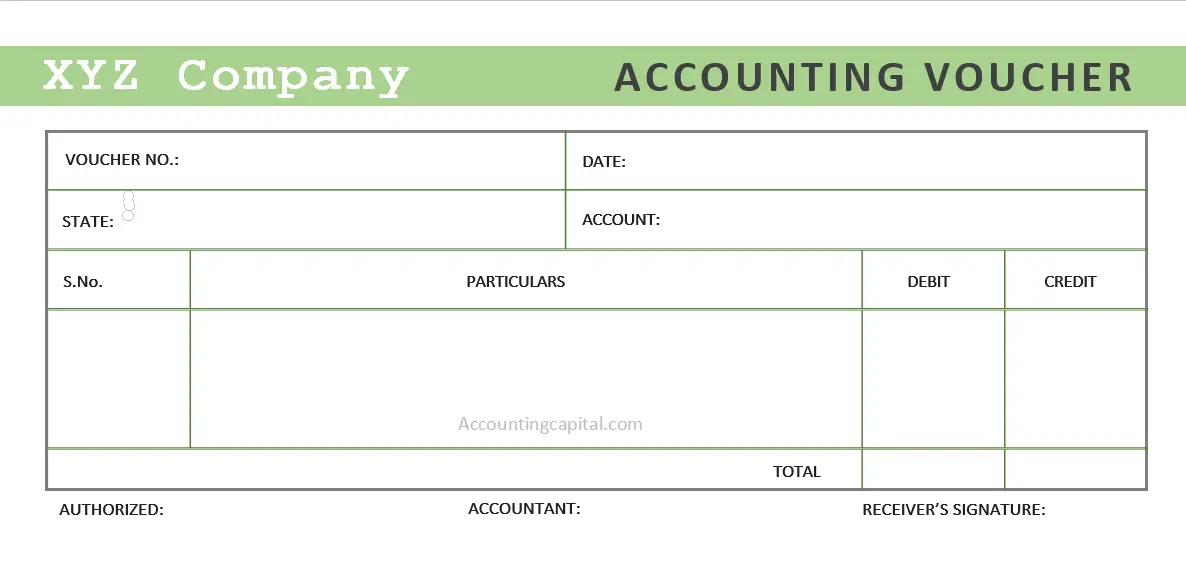

A document that serves as evidence for a business transaction is called a Voucher. Sometimes, mistakenly seen as just a bill or receipt; it can have many other forms.

It is not the appearance of it that matters it just needs to act as evidence of a transaction. When a transaction is entered, the evidence of that transaction is also confirmed. A voucher helps in recording expenses or liability and further helps in its payment.

They are also called source documents as they help in identifying the source of a transaction. A few examples of vouchers include bill receipts, cash memos, pay-in-slips, checks, an invoice, a debit or credit note.

Documents which are created at the time when a business enters into a transaction are called source vouchers, for example, rent receipts, bill receipts at the time of cash sales, etc.

They are expected to contain complete details of a transaction duly signed by the maker and act as evidence of the transaction.

Accounting Vouchers

This type of a voucher basically analyzes a business transaction from the accounting standpoint and is used for recording purposes.

These are commonly prepared by accountants on the basis of supporting vouchers and approved by a different individual. They are further subdivided into two, cash and non-cash vouchers.

We faced problems while connecting to the server or receiving data from the server. Please wait for a few seconds and try again.

If the problem persists, then check your internet connectivity. If all other sites open fine, then please contact the administrator of this website with the following information.

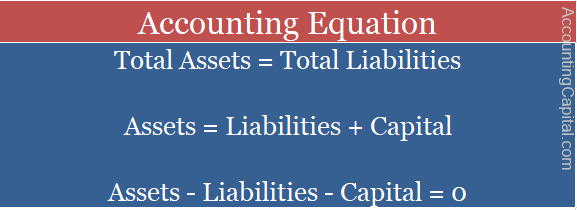

It wouldn’t be wrong to say that this equation is the basis of all accounting. The Accounting Equation is based on the dual aspect concept of accounting, which says that every transaction has two aspects, debit and credit, and for every debit, there is equal and opposite credit.

This equation is also called the Balance Sheet Equation. It helps to prepare a balance sheet, which is the most vital step in creating financial statements.

This relationship between Assets, Capital and Liabilities is called the Accounting Equation or the Balance Sheet Equation. In general, the expression Assets = Capital + Liabilitiesis termed as the Accounting Equation, but you can use any of the above relationships till the time you understand the fundamentals of the equation.

Therefore, at any point, the total number of assets of a firm is equal to the total number of liabilities. That is because the equation indicates that sources of funds are equal to the uses of funds. In other words, the equation means that capital and liabilities together are equal to assets at all times.

Key Highlights

The accounting equation acts as a basis for accounting and uses the dual aspect principle of accounting.

It is also known as the Balance Sheet Equation.

According to the balance sheet equation, total assets are always equal to the sum of capital and external liabilities.

Application and Integrity of the Accounting Equation

In the below-mentioned example, we will deal with 2 different transactions that took place in a newly started business called Unreal Pvt Ltd. This example will help you clearly understand how a transaction affects the variables involved in an accounting equation and still maintains the integrity of the equation.

1. Unreal Pvt Ltd. startsa business with 1,000,000 cash (1 Million)

Variables Affected

Net Effect of Transaction

Accounting Equation

Capital & Assets

Assets & Capital Both Increase

Assets = Liabilities + Capital

1,000,000 (cash) = 0 + 1,000,000

Starting a business with 1 million means that the business owner introduced capital or in other words owner’s equity is 1M, which, in this case, was brought inside the business in the form of cash. Therefore, their cash increased by 1M and capital also increased simultaneously by the same amount.

2. They purchase raw material for 50,000 cash

Variables Affected

Net Effect of Transaction

Accounting Equation

Only Assets

Raw material (Asset) increases and Cash (Asset) decreases by 50k

Assets = Liabilities + Capital

1M + 50k – 50k (Cash) = 0 + 1M

Unreal Pvt Ltd began operations by purchasing raw material for their business for 50,000 in cash. This transaction ultimately reduced 50k worth of cash and added 50k worth of raw material to the business.

Similarly, when other more complex transactions take place in business, the accounting equation will get affected each time, but it would still maintain its basic fundamental of assets being equal to the sum of capital and liabilities.

Short Quiz for Self-Evaluation

Loading

Your quiz has been submitted

Want to re-attempt? - “Refresh” this page.

Check out more content on our site :)

Subscribed? - Check your mailbox

Thank You!

Server Side Error

We faced problems while connecting to the server or receiving data from the server. Please wait for a few seconds and try again.

If the problem persists, then check your internet connectivity. If all other sites open fine, then please contact the administrator of this website with the following information.

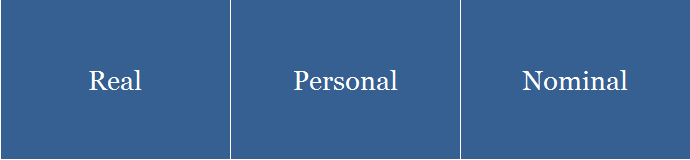

In accounting, an account is a specific header created for grouping similar transactions. It is maintained in a T-shaped tabular format with multiple columns containing matching transactions that are recorded together. Following the traditional approach, there are three types of accounts in accounting: Real, Personal, and Nominal.

They are journalized as per the golden rules of accounting. After that, the balance is transferred in a T-shaped table that contains all debit transactions on the lef, and the right-hand side includes all credit transactions.

Different types of financial statements are created using transactional information from accounts. A company’s financial position, operational performance, etc., are all represented using the same data.

As per the two accounting approaches i.e. the traditional (aka English approach) and the modern (aka American or the Accounting Equation approach) the accounts are classified into 2 major groups as shown below:

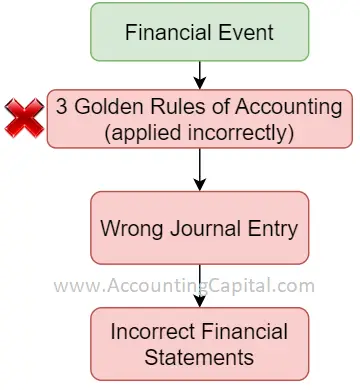

It is important to know what type of account are you dealing with because if you fail to identify an account correctly as either a real, personal or nominal account, in most cases, you will get end up recording incorrect journal entries.

A company’s financial data becomes unreliable when debit and credit rules are incorrectly applied. The golden rules are dependent on the accurate classification of the account.

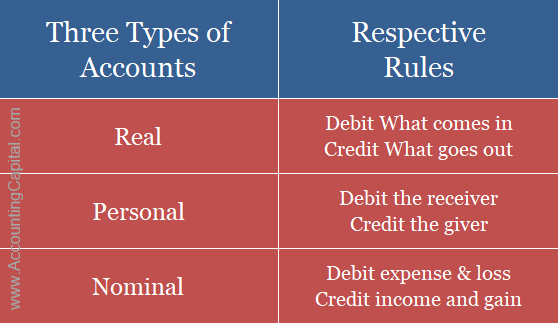

Three Types of Accounts

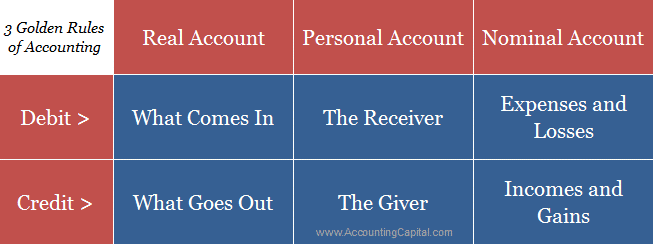

1. Real Accounts

All assets of a firm, which are tangible or intangible, fall under the category of ‘Real Accounts’. (Except debtors)

Tangible real accounts are related to things that can be touched and felt physically. A few examples of tangible real accounts are building, furniture, equipment, cash in hand, land, machinery, stock, investments, etc.

Intangible real accounts are related to things that can’t be touched and felt physically. A few examples of such real accounts are copyrights, intellectual property, customer data, goodwill, patents, trademarks, broadcasting rights, logos, etc.

The golden rule for real accounts

Debit What Comes in

Credit What Goes Out

Example of Real Accounts

The transaction below shows the interaction of two different accounts: one is ‘Furniture’ and the other is ‘Cash’.

Furniture – Real Account (tangible) & Cash in Hand – Real Account (tangible)

Purchased furniture for 10,000 in cash

Accounts Involved

Debit/Credit

Rule Applied

Furniture A/C

10,000

Real A/C – Dr. what comes in

To Cash A/C

10,00

Real A/C – Cr. what goes out

Important to know about Real Accounts – In spite of the fact that “debtors” are assets for the company, they continue to be classified as personal accounts. This is because ‘debtors’ belong to individuals or entities and personal accounts specifically serve the purpose of calculating balances due to or due from such 3rd parties.

Second among three types of accounts are personal accounts which are related to individuals, firms, companies, etc. A few examples are debtors, creditors, banks, outstanding accounts, prepaid accounts, accounts of customers, accounts of goods suppliers, capital, drawings, etc.

Natural personal accounts: All of God’s creations are included in these types of personal accounts. Accounts that belong to individuals fall into this category e.g. Kumar’s A/c, Adam’s A/c, Unreal Co. A/c, etc.

Artificial personal accounts:Personal accounts which are created artificially by law, such as corporate bodies and institutions, are called artificial personal accounts. E.g. private companies, LLCs, LLPs, clubs, schools, sole proprietors, public limited companies, one-person companies, cooperative societies, etc.

Representative personal accounts: These are accounts that directly or indirectly represent a particular person or a group of people.

Consider the example of an employee whose wages are paid in advance to him/her, a prepaid wages account will be opened in the books of accounts. This wages prepaid account is a representative personal account indirectly linked to the person.

A few other examples that are related are as follows: prepaid insurance account, unearned interest account, rent received account, accrued commission account, prepaid rent account, outstanding rent, etc.

The golden rule for personal accounts

Debit the receiver

Credit the giver

Example of Personal Accounts

The transaction below demonstrates the interaction between two accounts: one is a ‘Private Limited Company’ and the other is a ‘Bank’.

Private Ltd Co. – Personal Account (artificial) & Bank – Personal Account (artificial)

Accounts which are related to expenses, losses, incomes or gains are called Nominal accounts.

The dictionary meaning of the word ‘nominal’ is “existing in name only“ and the meaning is absolutely true in the accounting terms as well. There is no physical existence of nominal accounts, but money is involved behind every such account even though they have no physical form.

Example – Purchases, Sales, Salaries,Commission Received, Bad Debts, Telephone Bills, etc. The final result of all nominal accounts is either profit or loss which is then transferred to the capital account.

The golden rule for nominal accounts

Debit all expenses and losses

Credit all incomes and gains

Example of Nominal Accounts

The transaction below shows the interaction between two accounts: one is a ‘Purchase’ and the other is ‘Cash’.

*Persons – Our use of the word “persons” mirrors the usage found in the financial world. In this context, it can refer to individuals, firms, companies, etc.

It is nearly impossible to provide a complete list of accounts therefore we tried to provide you with the most often used accounts along with a general understanding of how similar types of accounts may look like.

We have created a printer-friendly PDF version of the above table that can be instantly downloaded, for free. Those who use the three types of accounts in accounting and apply the legacy rules of debit and credit regularly should print or save this on their desktop.

We faced problems while connecting to the server or receiving data from the server. Please wait for a few seconds and try again.

If the problem persists, then check your internet connectivity. If all other sites open fine, then please contact the administrator of this website with the following information.

Do not miss our 1-minute revision video. This will help you quickly revise and memorize the topic forever. Try it :)

Practice

This section is dedicated to the practice of the three types of accounts in accounting. Practising this will help you gain a better understanding of the subject.

Question – Identify the accounts involved and their types. Also, state whether they should be debited or credited.

1. Paid rent for 30,000 in cash.

Accounts Involved – Rent Expense A/c & Cash A/c

Type – Rent Expense is a Nominal account & Cash is a Real account

Debit & Credit – Rent Expense A/c will be debited by 30,000 (Dr. all expenses & losses) whereas Cash A/c will be credited by 30,000 (Cr. what goes out)

2. Mary started the business with 95,000 in cash.

Accounts Involved – Cash A/c & Capital A/c

Type – Cash is a Real account & Capital A/c is a Personal account

Debit & Credit – Cash A/c will be debited by 95,000 (Dr. what comes in) whereas Capital A/c will be credited by 95,000 (Cr. the giver)

Capital A/C and Mary’s Capital A/C both can be used in the above question.

3. Sold goods on credit to Unreal Company for 25,000

Type – Unreal Company’s A/c is a Personal account & Sales is a Nominal account

Debit & Credit – Unreal Company’s A/c will be debited by 25,000 (Dr. the receiver) whereas Sales A/c will be credited by 25,000 (Cr. all incomes & gains)

4. Purchased goods on credit from Kumar for 50,000

Type – Purchases A/c is a Nominal account & Kumar’s A/c is a Personal account

Debit & Credit – Purchases A/c will be debited by 50,000 (Dr. all expenses & losses) whereas Kumar’s A/c will be credited by 50,000 (Cr. the giver)

5. 40,000 cash withdrawn by the proprietor for personal use

Accounts Involved – Drawings A/c & Cash A/c

Type – Drawings A/c is a Personal account & Cash A/c is a Real account

Debit & Credit – Drawings A/c will be debited by 40,000 (Dr. the receiver) whereas Cash A/c will be credited by 40,000 (Cr. what goes out)

6. Paid 2,000 as carriage inwards by cheque (inventory purchase)

Accounts Involved – Carriage Inwards A/c & Bank A/c

Type – Carriage Inwards A/c is a Nominal account & Bank A/c is a Personal account

Debit & Credit – Carriage Inwards A/c will be debited by 2,000 (Dr. all expenses & losses) whereas Bank A/c will be credited by 2,000 (Cr. the giver)

“Purchases account” is also debited (equal to the amount of purchase), however, it is not necessary to show that in the above practice example. Carriage inwards is treated as a direct operating expense since the product is intended for operational use.

7. Commission received 80,000 in cash

Accounts Involved – Cash A/c & Commission Received A/c

Type – Cash A/c is a Real account & Commission Received A/c is a Nominal account

Debit & Credit – Cash A/c will be debited by 80,000 (Dr. what comes in) whereas Commission Received A/c will be credited by 80,000 (Cr. all incomes & gains)

8. Paid 15,000 by the bank for trademark registration

Accounts Involved – Trademark A/c & Bank A/c

Type – Trademark A/c is a Real account & Bank A/c is a Personal account

Debit & Credit – Trademark A/c will be debited by 15,000 (Dr. what comes in) whereas Bank A/c will be credited by 15,000 (Cr. the giver)

Although a trademark may seem like an expense, it is an intangible asset and should not be viewed as a nominal account.

Type – Depreciation A/c is a Nominal account & Furniture A/c is a Real account

Debit & Credit – Depreciation A/c will be debited by 15,000 (Dr. all expenses & losses) whereas Furniture A/c will be credited by 15,000 (Cr. what goes out)

Depreciation is a non-cash expense and should be viewed as a nominal account. The amount debited & credited should be equal to the depreciation expense.

14. Received 7,000 as interest on drawings from Neel (Proprietor)

Accounts Involved – Drawings A/c & Interest on Drawings A/c

Type – Drawings A/c is a Personal account & Interest on Drawings A/c is a Nominal account

Debit & Credit – Drawings A/c will be debited by 7,000 (Dr. the receiver) whereas Interest on Drawings A/c will be credited by 7,000 (Cr. all incomes & gains)

Due to the fact that interest on drawings is an income for the company, it is added to the company’s interest account, thereby increasing its income. Actual cash is not received, instead, adjustments are made within relevant accounts.

15. 9,500 received in cash from Unreal Co. as the full and final settlement of their account worth 10,000.

Cash is a Real account so Dr. what comes in (9,500), Discount Allowed A/c is a Nominal account so Dr. all expenses/losses (500), and Unreal Co. A/c (Debtor) is a Personal account so Cr. the giver (10,000).

Type – Cash A/c is a Real account, Discount Allowed A/c is a Nominal account, and Unreal Co. A/c (Debtor) is a Personal account.

Debit & Credit – Cash A/c will be debited by 9,500 (Dr. what comes in), Discount Allowed A/c will be debited by 500 (Dr. all expenses & losses) whereas Unreal Co. A/c will be credited by 10,000 (Cr. the giver)

Accounts are broken down into 2 major categories based on their type, according to the traditional approach: Personal, and Impersonal. Personal accounts come in three types. Impersonal accounts are further broken down into two: Real & Nominal.

Due to its more holistic approach, the modern classification of accounts (assets, liabilities, revenue, expenses & capital) has gained more followers than the traditional classification (real, personal & nominal).

As far as we are concerned, using modern rules and classifications is easier and more convenient than using traditional rules.

There are some tricky cases where a person might incorrectly identify an account and we would like to identify them explicitly.

Accrued Income – is a personal account whereas the related income account is a nominal account. Any income or expense with a prefix such as prepaid, outstanding, accrued, received in advance, etc. shall be classified as a personal account.

Bank – It is easy to get confused because a bank account may seem like an asset therefore it should be a real account, No! Due to the fact that the bank account belongs to a legal entity, it is considered a personal account & treated accordingly.

Capital or Equity – It is a personal account as equity/capital is provided to the company by a person i.e. individual, firm, company, etc.

Goodwill – At the time of comparing tangible and intangible assets, it is easy to forget that assets are both physical and non-physical therefore, all intangible assets like goodwill, copyright, patents, investments, etc. are categorized as real accounts.

Drawings – Drawings refer to withdrawals of cash or goods for personal use by the owners of a business. Since the owner is a separate entity from the business, it is seen as a personal account.

Debtors – It’s easy to get confused because debtors are receivables, which are assets, so it should be treated as a real account, No! Due to the fact that debtors are an external third party (a separate entity), they are treated as personal.

The debit and credit rules are applied correctly when the type of account is accurately identified. By doing this, all financial events of a business are accurately recorded and accounted for. As a result, in the light of the accounting equation, debits are always equal to credits and the balance sheet is always a match.

Due to the fact that both internal and external users of accounting information rely on financial data, the accounts identified and the resulting rules applied should be accurate at all times.

In the general sense of the English language, something described as “Golden” means prime quality. In the context of accounting, the golden rules are the main rules used to record financial transactions at the time of their inception. These rules determine which accounts should be debited and credited.

A journal entry is the foundation of the financial statements of a company. Financial data becomes unreliable when debit and credit rules are incorrectly applied. Financial statements, for example, are based on trustworthy accounting data that is backed up by this rule and other accounting principles.

Each accounting entry is recorded chronologically in “the book of original entry” (journal or subsidiary books) according to the 3 golden rules of accounting.

Source documents are used to support the entry of transactions in the books of account. For example; invoices, cheques, receipts, debit notes, credit notes, etc.

After the activity has been recorded the next step is to ‘post’ the entry i.e. transfer it to the appropriate ledger account.

What is an account? – It is kind of a table in “T” form where transactions are recorded under specific headings. The data is not only used to track the amount of a transaction but also its effect and direction as well.

On the left-hand side, you will find all the debit transactions, and on the right-hand side, you will see all the credit transactions.

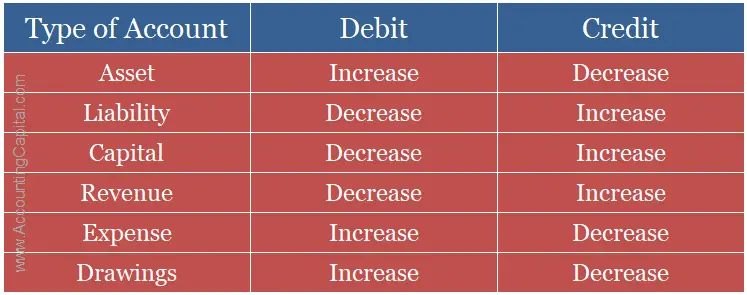

Debit & Credit – According to the nature of an account, it could mean either an increase or a decrease. Debits and credits are governed differently depending on the account type.

Debit – It means an increase in the value of an asset or expense or a decrease in the value of liability (including equity) or revenue.

Credit – It is the opposite of debit and it means a decrease in the value of an asset or expense or an increase in the value of liability (including equity) or revenue.

These rules are used to prepare an accurate journal entry that forms the basis of accounting and acts as a cornerstone for all bookkeeping.

They are also known as the traditional rules of accounting or the rules of debit and credit.

Easy Interpretation of 3 golden rules of accounting

Real Account

If the item (real account) is coming into the business then – Debit

If the item (real account) is going out of business then – Credit

Personal Account

If the person (or) legal body (or) group is receiving something – Debit

If the person (or) legal body (or) group is giving something – Credit

Nominal Account

If it is an expense or loss for the business – Debit

If it is an income or gain for the business – Credit

While making a journal entry there are essentially three types of accounts i.e. Real, Personal and Nominal. Each account has a specific rule that needs to be applied and it is of utmost importance to identify the account correctly for accurate journalisation.

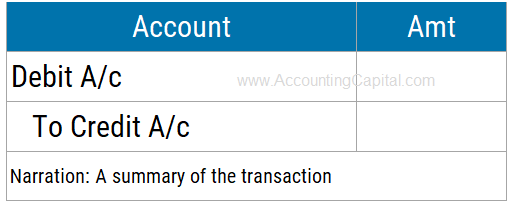

When recording a journal entry, one must adhere strictly to the golden rules of accounting in order to ensure that the entry is accurately recorded. The following steps are used to register an entry in the primary book of accounting:

Identify the accounts involved

Determine the type of accounts

Apply the golden rules of accounting

Record the Transaction

Here is an example to help you understand. This example shows a business receiving cash and making a sale.

Cash A/c

Debit

Real – Debit what comes in

To Sales A/c

Credit

Nominal – Credit all income/gain

Step 1 – The first step of a journal entry is to identify the accounts involved in a transaction. A minimum of two such accounts shall be identified. According to the above example, the two accounts affected are “Cash” and “Sales”.

Step 2 – After identifying the type of accounts in step 1, the next step is to determine their type (real, personal, or nominal). According to the above example, the two accounts affected are “Cash” which is a real account and “Sales” which is a nominal account.

Step 3 – The highlight of our topic is the application of golden rules. It should be done correctly after determining the type of accounts.

As per the three rules of debit and credit (shown below) “Cash A/c” (Real) should be treated as per the 1st rule since cash is coming into the business “Debit what comes in”.

Similarly, “Sales A/c” should be treated as per the 3rd rule since the sale is an income for the business “Credit all incomes & gains”.

Rules of Debit and Credit According to Modern Approach

If you are posting an entry in the journal, you may use the Modern Accounting Approach instead of the three golden rules of accounting.

You should try to use the American or modern rules of accounting to compare and find out which one suits your learning style and is easy to apply. It is true that some people find the modern approach easier than the traditionally used three golden rules of accounting.

Example – Modern Rules of Accounting

Received cash 3,000 as rent from Unreal Pvt Ltd.

Accounts Involved

Debit/Credit

Modern Rule Applied

Cash A/C

3,000

Asset A/C – Dr. the increase

To Rent A/C

3,000

Revenue A/C – Cr. the increase

Short Quiz for Self-Evaluation

Loading

Your quiz has been submitted

Want to re-attempt? - “Refresh” this page.

Check out more content on our site :)

Subscribed? - Check your mailbox

Thank You!

Server Side Error

We faced problems while connecting to the server or receiving data from the server. Please wait for a few seconds and try again.

If the problem persists, then check your internet connectivity. If all other sites open fine, then please contact the administrator of this website with the following information.

Do not miss our 1-minute revision video. This will help you quickly revise and memorize the topic forever. Try it :)

Practice

This section is dedicated to the practice of the three golden rules in accounting. Practising this will help you gain a better understanding of the subject.

Question – For 1 to 10, give the nature of each account as well as the relevant rule to be applied. From 11 to 15, identify the accounts involved, along with their nature and the respective rules.

1. Cash

Type & Rule – Real A/c, Rule – Dr. what comes in and Cr. what goes out

Cash is an asset for the business and all assets (tangible and intangible are real accounts)

2. Loco Pvt Ltd. (Debtor)

Type & Rule – Personal A/c, Rule – Dr. the receiver and Cr. the giver

It is important to understand that a debtor is not categorized as a real account even though it is an asset to the business, however, it is classified as a personal account because it belongs to an individual or entity. A personal account is used to determine a person’s or organization’s balance due.

3. Goodwill

Type & Rule – Real A/c, Rule – Dr. what comes in and Cr. what goes out

It is treated as a real account since it is an asset to the business.

4. Purchases

Type & Rule – Nominal A/c, Rule – Dr. all expenses and losses & Cr. all incomes and gains

Purchases are an expense for the business therefore it is a nominal account.

5. Bank

Type & Rule – Personal A/c, Rule – Dr. the receiver and Cr. the giver

It is easy to confuse the Bank as a real account whereas it is actually categorized as a personal account because it belongs to an entity.

6. Inventory

Type & Rule – Real A/c, Rule – Dr. what comes in and Cr. what goes out

As a business asset, it is treated as a real account.

7. Salaries

Type & Rule – Nominal A/c, Rule – Dr. all expenses and losses & Cr. all incomes and gains

Salaries are an expense for the business therefore it is a nominal account.

8. Outstanding Salaries

Type & Rule – Personal A/c, Rule – Dr. the receiver and Cr. the giver

Salaries are an expense for the business whereas outstanding salaries are related to a worker or several workers which means the o/s salary account becomes a personal account. The thumb rule in the case of a prefix or suffix (outstanding, prepaid, accrued, etc.) is the type of account changes from nominal to personal.

Type & Rule – Real A/c, Rule – Dr. what comes in and Cr. what goes out

A leaseholder has the right to use the property for a specified period of time according to a lease agreement. An extremely low down payment is made by the lessee to acquire and use the property. Such a property is treated as a real account since it is a business asset.

10. Bad Debts Written Off

Type & Rule – Nominal A/c, Rule – Dr. all expenses and losses & Cr. all incomes and gains

The write-off of bad debts is the act of writing off receivables which the company now considers irrecoverable. It should be shown on the income statement and removed from the books of accounts. Since it is a loss for the business, it is treated as a nominal account.

11. Sold goods for cash 50,000

Accounts Involved – Cash A/c & Sales A/c

Type and Rules – Cash is a Real account so Dr. what comes in (50,000), Sales is a Nominal account so Cr. the income (50,000).

Type and Rules – Unreal Co. A/c is a personal account so Dr. the receiver (11,000), Sales is a Nominal account so Cr. the income (11,000).

It is important to note that in the above question the business is dealing with another entity. The account will be categorized as personal even though it is an asset for the firm.

13. Purchased Equipment for 10,000 (paid by Cheque)

Accounts Involved – Equipment A/c & Bank A/c

Type and Rules – Equipment A/c is a real account so Dr. what comes in (10,000), Bank is a personal account so Cr. the giver (10,000).

In many cases, a bank account is mistaken for a real account, when in fact it is a personal account because it belongs to a separate business entity.

14. Paid Salaries of 90,000 (Direct Deposit from Bank)

Accounts Involved – Salaries A/c & Bank A/c

Type and Rules – Salaries A/c is a nominal account so Dr. all expenses (90,000), Bank is a personal account so Cr. the giver (90,000).

15. 9,500 received in cash from Unreal Co. as the full and final settlement of their account worth 10,000. (Compound Journal Entry)

When many accounts are debited or credited, it is called a compound journal entry. As opposed to a simple journal entry that only includes a maximum of 1 debit and 1 credit. Usually, such an entry has 3 or 4 affected accounts.

Type and Rules – Cash is a Real account so Dr. what comes in (9,500), Discount Allowed A/c is a Nominal account so Dr. all expenses/losses (500), and Unreal Co. A/c (Debtor) is a Personal account so Cr. the giver (10,000).

We have created a printer-friendly PDF version of the rules. For those who use the golden rules of accounting regularly, it is highly recommended that they print this page and stick it on their desk or wall.

The three golden rules of accounting ensure that all the financial events of a business are accounted for and done accurately. As a result, in the light of the accounting equation, debits are always equal to credits and the balance sheet is always a match.

To ensure maximum financial transparency and accountability, businesses should ensure the implementation of these accounting principles and standards.

The customer accounts (debtors) who owe money to a business for purchasing goods on credit are called accounts receivable. When the money is received within the same accounting period it becomes part of the company’s operating revenue, however, if not received in the same year it becomes “trade debtors” which is another name for accounts receivable. It is also commonly abbreviated as “AR”. The entire life-cycle is termed as “O2C” (Order to Cash).

In layman terms, the total amount which is yet to be collected by debtors as per a firm’s sales book is known as accounts receivables. Large firms using ERP packages replace traditional sales book with sales ledger control account.

The buyer can be a sole trader, a partnership firm, a private company, etc. It is a short-term addition, hence an asset that is supposed to be received from the customers. Accounts receivables are shown on the asset side under the head current assets (right-hand side of a horizontal balance sheet).

Let us assume that you sold goods worth 10,000 to one of your buyers who is supposed to pay you within 45 days of receipt of invoice. Now, you send the customer a bill for 10,000. In this case, the amount acts as “dues to be received” and shall be booked in your records as accounts receivable.

It is similar to the situation where your mobile phone company generates an invoice on the 1st day of a month and gives you 30 days to pay the bill. It is an account receivable for the mobile phone company.

Key Highlights

They are created when a business sells goods on credit.

They should be collected from the customers within the agreed period.

If goods are returned by the buyer during the allowed time limit then a credit note is sent by the seller to notify the buyer that he has been provided appropriate credit. This cancels out his payment & results in a reduction of total accounts receivable.

Journal Entries Related to Accounts Receivable

Below are the two main scenarios linked to accounts receivable cycle where, in the first case, credit sale is recorded and the customer is assumed to be billed, and, in the second case, cash proceeds from the customer is recorded in books of accounts.

At the time of recording a credit sale and billing the customer

Accounts Receivable A/C

Debit

To Sales (on credit) A/C

Credit

(This can also be recorded at a particular customer level subledger wise, in that case, the customer who is billed will be debited)

(This can also be recorded at a particular customer level subledger wise, in that case, the customer paying for the goods/services will be credited)

Short Quiz for Self-Evaluation

Loading

Your quiz has been submitted

Want to re-attempt? - Simply “refresh” this page.

Please check out more content on our site :)

Subscribed? - Check your mailbox

Thank You!

Server Side Error

We faced problems while connecting to the server or receiving data from the server. Please wait for a few seconds and try again.

If the problem persists, then check your internet connectivity. If all other sites open fine, then please contact the administrator of this website with the following information.

Accounts payable are obligations of a business that originate because of purchases made on credit (e.g. for raw material, finished goods etc.), the money is yet to be paid for these transactions. Accounts payable account can be created by anyone who buys goods or services on credit and promises to pay for them later. It can be a sole trader, a partnership firm or a full-fledged business.

It is a short-term liability and in simpler terms total amount which is yet to be paid by the business to its creditors as per the purchase book. Large firms using ERP packages replace traditional purchase book with purchase ledger control account.

It is also known as trade creditors, “AP” & “P2P” (Procure to Pay). Accounts payable are shown on the liability side under the head current liabilities (the left-hand side of a horizontal balance sheet).

Let us say a supplier extends credit to your business Unreal Pvt Ltd. and agrees that your business will be making a payment within 45 days of the date you are billed.

Now, you are billed 1,00,000 for goods bought on credit. The amount will be considered as dues to be paid or, in other terms, an “account payable” by your business till the supplier is paid. It is similar to the situation when a person has received his latest electricity bill where he is allowed to pay within the next 30 days. Now, it acts as payable for the individual until the time it is actually paid.

Key Highlights

Accounts payable are created when you buy goods on credit.

Accounts payable should be paid back to the suppliers within the agreed period of time.

They act as short-term debt, hence shown on the liability side under the head “current liabilities” of the balance sheet.

Journal Entries Related to Accounts Payable

Below are two main scenarios linked to the accounts payable cycle, where, in the first case, the credit purchase is recorded, and, in the second case, the cash paid to the supplier is recorded in the books of accounts.

At the time of recording an invoice

Purchase A/C

Debit

To Accounts Payable A/C

Credit

(This can also be recorded at a particular vendor level subledger wise, in this case, the vendor who has raised the invoice will be credited)

At the time of paying an invoice

Accounts Payable A/C

Debit

To Cash or Bank A/C

Credit

(This can also be recorded at a particular vendor level subledger wise, in this case, the vendor paid will be debited)

Short Quiz for Self-Evaluation

Loading

Your quiz has been submitted

Want to re-attempt? - Simply “refresh” this page.

Please check out more content on our site :)

Subscribed? - Check your mailbox

Thank You!

Server Side Error

We faced problems while connecting to the server or receiving data from the server. Please wait for a few seconds and try again.

If the problem persists, then check your internet connectivity. If all other sites open fine, then please contact the administrator of this website with the following information.

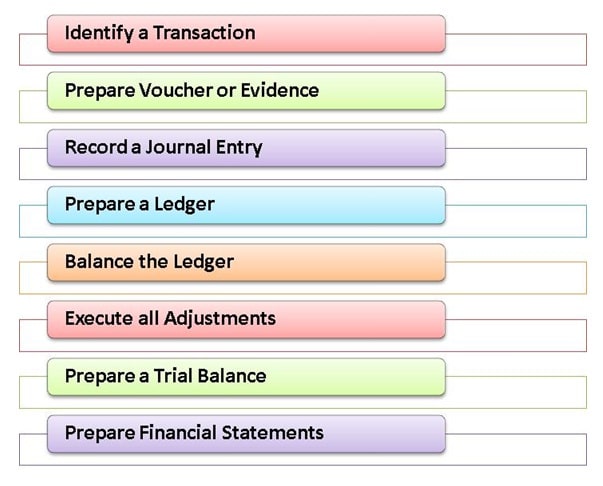

The accounting cycle is a chronological order in which an accounting process flows. It is a step by step process followed to achieve the ultimate goals of accounting.

Firstly, the information is recorded in a book or accounting software (in the modern scenario) called a Journal. Then it is adjusted and moved to a ledger. Ledger balances are then summarized to make a trial balance. Finally, from trial balance financial statements such as an income statement, a trading account, and a balance sheet are prepared.

Accounting Cycle Steps

Identification – This is the origin of the accounting cycle. This step means identifying events that are to be recorded. It involves observing activities and selecting those events that are – considered to be evidence of economic activity and are relevant to the business organization. So, Events that are relevant and can be quantified in monetary terms are considered for the recording.

Prepare Evidence – When a financial transaction occurs, it gives rise to a source document. This supply document is proof that describes all the fundamental facts of the transaction in question, as the amount, which parties are involved, the aim of the transaction, and the transaction date. Thus, documents such as; a receipt, an invoice, a depreciation schedule, and a bank statement, a debit note, a credit note, etc. produce proof that an economic event has actually occurred.

Record a Journal Entry – Once the economic events are identified and quantified, this step involves recording transactions in chronological order and a systematic manner. According to double-entry accounting, each transaction should be recorded as both a credit and debit in separate journals. Sometimes, transactions are recorded in the books of original entries also.

Prepare a Ledger – Ledger accounts keep track of a company’s entire financial activity. Record of the journal and other subsidiary books is input for the ledger. Under this step, posting is done in the ledger in various accounts, on the basis of Journal entries.

Balance the Ledger – Each account like cash, accounts payable, investments, inventory, etc are balanced at the end of a certain period. If the total of the debit side is more than that of the credit side, the balance is called Debit Balance and is written on the credit side. In the same way, when the total of the credit side of an account is more than that of the debit side total, the balance is called Credit Balance. The difference amount is written on the debit side of the account. So, these balances are the output of this step.

Execute Adjustments – At the end of the period, adjustments are made. These are the result of rectifications made in the books of accounts and the results from the passage of time. For example, an adjusting entry may include advance payment of rent or insurance. So, this step requires the usage of the matching principle to organize company transactions into the appropriate financial periods.

Prepare Trial Balance– Balances from the ledger are brought to the trial balance. This is done so that any mathematical errors that may have occurred during the initial stages of the accounting cycle, can be identified. A trial balance matches if the total of debit is equivalent to the total of credit for the business.

Prepare Financial Statements – The last step of the Accounting cycle allows the organization of relevant financial data into appropriate categories in the financial statements of the business. Record of the trial balance is the input for this step. It involves summarizing transactions into Trading Account, Profit & Loss Account, and Balance sheet based on their nature.

Example of Accounting Cycle

PepsiCo bought a new processing plant for 10 Million, which was shown on the balance sheet as an asset. We will study the possible accounting trail related to this transaction.

Step 1

Transaction for buying the building is identified.

Analysis – Buying a new plant is both relevant for the business and can be quantified in monetary value. So, this is an economic activity.

Step 2

Evidence such as a legal ownership document is prepared.

Analysis – The ownership deed is the source document that will be evidence for the above financial transaction. It will disclose the parties involved, amount and time of transfer of payment, etc.

Step 3

Journal entry to purchase the building is recorded in books.

Analysis – A Journal entry to record the transaction will be passed. PepsiCo now has more plant than before. The plant is an asset, which is increasing on the debit side for 10 million. If a Bank transfer is done to pay for it, the bank balance is an asset, decreasing on the credit side.

Step 4

A ledger account such as a “Plant & Equipment account” is created.

Analysis – PepsiCo will go through each transaction and transfer the account information into the debit or credit side of that ledger account being affected. In the Plant & Equipment Account, there will be a debit of Bank by 10 million.

Step 5

Ledger account for the Plant & Equipment is then balanced.

Analysis – If there are no further transactions, the Ledger account is balanced and shows a debit balance.

Step 6

All adjustments, if any, are incorporated.

Analysis – If there is a requirement for rectifications, adjustment entries will be passed.

Step 7

The amount is treated as an asset and moved to trial balance.

Analysis – The balance of the Ledger account is the nature and output for the Trial Balance. The plant is treated as an asset and the ledger balance is its historical value.

Step 8

The amount is then shown on the asset side of the balance sheet.

Analysis – Since the above transaction involves two assets (Plant & Bank balance) only, it will reflect in the balance sheet. The Balance sheet will show an enhanced value of plant and reduced value of bank balance by 10 million.

Short Quiz for Self-Evaluation

Loading

Your quiz has been submitted

Want to re-attempt? - “Refresh” this page.

Check out more content on our site :)

Subscribed? - Check your mailbox

Thank You!

Server Side Error

We faced problems while connecting to the server or receiving data from the server. Please wait for a few seconds and try again.

If the problem persists, then check your internet connectivity. If all other sites open fine, then please contact the administrator of this website with the following information.

According to the dual aspect principle of accounting, business is a separate independent entity. Double-entry accounting system includes receiving benefits from some sources and giving it to some others. Benefits received and benefits provided should always match and balance out.

Every transaction has two aspects debit and credit; two equal amounts. Every business transaction has 2 effects. In the case when there are multiple accounts involved (compound journal entry), the total of debit entries must be equal to the total of credit entries.

Every transaction has 2 sides;

1. The receiver of the benefit

2. Giver of the benefit

In all cases, Benefit Received = Benefits Provided

Example – Double Entry Accounting

Let us assume that a business purchases a building for 1,000,000, In this transaction, the business receives the ownership of the building and gives 1,000,000 to the seller.

The benefit received by the business is equal to the benefit given, which in this case sums up to 1,000,000.

A complete record of transactions, i.e. both sides of a transaction, give and take, are recorded, which in its turn helps to have a clear and much accurate image of a business’ profit or loss.

A comparison becomes possible as financial statements of one year can be easily compared with previous periods which can further help analyze upturns and downturns.

Accuracy is also enhanced by the double-entry system as it becomes possible to build a trial balance to try both the debit and the credit balances.

A double-entry system is a full proof scientific system as it records both sides of a transaction and no other system provides this level of accuracy.

Also known as accounts from incomplete records, this type of accounting system is also called an incomplete double-entry system. A few transactions are recorded on the single side, a few – on the double side and some are not recorded at all. Only cash book and personal accounts are maintained under this system. None of the accounts under this system is reliable.

Under a single entry accounting system, you can’t prepare a trial balance, income statement, and balance sheet.

Short Quiz for Self-Evaluation

Loading

Your quiz has been submitted

Want to re-attempt? - “Refresh” this page.

Check out more content on our site :)

Subscribed? - Check your mailbox

Thank You!

Server Side Error

We faced problems while connecting to the server or receiving data from the server. Please wait for a few seconds and try again.

If the problem persists, then check your internet connectivity. If all other sites open fine, then please contact the administrator of this website with the following information.

There are general rules, guidelines and concepts in every field of study, accounting is no different. Accounting principles are accounting standards or rules that have been generally accepted. Based on these rules, accounting takes place and financial statements are made. If a company reports its financial statements to the public, it is expected to follow GAAP (Generally Accepted Accounting Principles) while preparing its financial statements.

Without the GAAP, companies would be free to decide for themselves what and how to report their financial information, making things quite difficult for investors and creditors who have invested in that company. GAAP makes a company’s financials comparable and understandable for investors, creditors and others to make intelligent decisions.

.

Principle of Income Recognition

It is also called the Revenue recognition concept. According to this concept, the income is considered to be earned on the date it is realized. In layman terms, income is considered as earned on the date when goods or services are transferred to a customer for cash or for a promise (credit). The terms of a contract between the buyer and the seller determine a point of sale. Generally, a sale is said to have been completed & ownership is considered to be transferred when goods are delivered to the buyer by the seller.

Key Highlights

It doesn’t matter when the cash is received for a particular transaction, the income will be recorded at the time of point of sale (POS).

Only revenue, which is realized, should be taken to the Income statement.

Example – Let us assume that a company Unreal Corporation sells goods worth 20,000 to one of its buyers in January YYYY, but gets paid for them in March YYYY. The income from this sale should be recorded in the month of January when the goods were sold, and not in March. This is because a legal obligation was made in January.

A different example is when Unreal Corporation has received an advancefor 20,000 in the month of January YYYY from one of its buyers for sales to be made in July YYYY. Now, in this case, the income would only be recognized in the month of July and not in January as the legal obligation is made in July.

Dual Aspect Principle

Also known as the Duality Principle, it is the most basic feature of an accounting transaction and is embodied in the double-entry system itself. This is linked to the business separate entity concept as a business is a separate, independententity, it receives benefits from some and gives benefits to some others. Benefits received and benefits provided should always match and balance out. Every transaction will have two aspects, a debit and a credit, of equal amounts.

Example –Let’s assume that Mr Unreal starts a business with 10,00,000 and buys a vehicle for 2,00,000 for official purpose. The current financial position of the business would be as follows:

Balance Sheet

Liabilities

Assets

Capital

10,00,000

Vehicle

2,00,000

Cash

8,00,000

10,00,000

10,00,000

The total liabilities are equal to the total assets. This is the dual aspect principle of accounting.

There were 2 aspects of each transaction mentioned in the example:

1. On one hand, the business gets an asset for 10,00,000 and on the other hand, has a liability of 10,00,000 towards Mr Unreal (Capital).

2. The second transaction, where Mr Unreal buys a vehicle for business priced 2,00,000, also has two effects: on one hand, it brings in an asset for 2,00,000 and on the other hand, it also reduces cash by 2,00,000 as a payment towards it.

Principle of Expenses

Expenses are not payments, a payment only becomes an expense when it is revenue in nature. It means that for a payment to be qualified as an expense, it has to be for consideration. All revenue expenses are transferred to the profit and loss account to ascertain profit or loss of the business undertaking. So, there are three different forms: revenue, expenses and capital payments. Revenue expenditure is charged against profits and is shown in the profit and loss account. However, capital payments are shown in the balance sheet as assets.

Example – Wages Paid is an example of an expense, where vehicle purchased for official purpose is an example of capital payment.

Modifying Principle

According to this principle, the cost of implementing a principle should not be more than the benefit derived from it. A cost and benefits analysis is necessary before applying the principle. If the cost is more than the benefit derived, then the principle should be modified. There should be flexibility in adopting a principle and the advantage out of the principle should overweigh the cost of implementing the principle.

One of the areas which govern the selection and application of accounting policy is

Substance over form: Transactions and events should be accounted for and presented in accordance with their substance and financial reality and not merely with their legal form. In accounting, the substance should normally take priority over form in deciding how a particular transaction should be recorded.

Example – Hire-purchase transactions are based on the substance over form principle, it looks at the substance of the transaction and not its legal form. The purchaser can record the asset at its cash down the price, while the payment for it can still happen as instalments over a pre-decided period of time.

Principle of Matching Cost and Revenue (Accruals)

The accrual or matching concept is an outcome of the periodicity concept. According to this principle, the expenses for an accounting period are matched against related incomes, instead of comparing the cash received and the cash paid. The revenue earned during a period is compared with the expenditure incurred to earn that income, whether the expenditure is paid in that period or not. This is called Accrual or the Matching Cost and Revenue Principle.

The principle is used to find the exact profit earned for that period. It is also important to give a true and fair view of the profitability and the financial position of a business.

Example

Sales Revenue in 2013

10,00,000

Expenses incurred in 2013

7,50,000

Out of the above, expenses to be paid in 2014 are

1,50,000

Net profit as per matching principle

10,00,000 – 7,50,000 = 2,50,000

*Even if 1,50,000 is due in 2014, it will still be considered as an expense for the year 2013.

Accruals are adjusted while preparing financial statements such as outstanding expenses, prepaid expenses, accrued income, and income received in advance.

Materiality Principle

The concept of materiality is the basis for recognizing a transaction in the entire process of accounting. Important details of the financial status must be provided to all relevant parties, insignificant facts which don’t influence any decisions of the investors or any interested party need not be communicated. According to the American Accounting Association, “an item should be regarded as material if there is a reason to believe that knowledge of the item would influence the decision of an informed investor“.