In personal finance, the dynamics of borrowing money are significantly influenced by fluctuations in Personal Loan interest rates. As interest rates rise, borrowers find themselves in a financial landscape where the cost of borrowing becomes a paramount concern. Let’s delve into the multifaceted impact of escalating Personal Loan interest rates on borrowers, exploring the challenges, considerations, and adjustments individuals must grapple with in the face of this financial shift. Understanding these implications is essential for anyone navigating the borrowing landscape and striving to make informed financial decisions amidst changing interest rate scenarios.

When Do Personal Loan Interest Rates Increase?

Financial institutions increase their Personal Loan interest rates when the RBI increases their repo rate. A higher repo rate means rising borrowing costs for the loan company. As a result, they increase the interest rate they charge their borrowers. However, the impact of rising interest rates will largely depend on the type of loan interest rate.

There are two types of interest rates: fixed and floating. If you borrow a fixed-rate loan, your interest rate is set at the time of borrowing and remains the same throughout the loan tenure. However, if your loan has a floating interest rate, it will fluctuate during the loan term according to the market conditions. That means if the RBI increases the repo rate, your interest rate will also increase and impact your monthly installments.

Impact of Increasing Interest Rates on Existing Personal Loans

Most Personal Loan plans have fixed interest rates. Since your rate is locked for the loan duration, fluctuating interest rates will not impact your monthly repayments. However, rising interest rates will result in bigger EMIs for variable-rate loans. When the repo rate increases, the financial institutions may raise their rates to account for the extra expense. Consequently, borrowers must adjust bigger EMIs into their monthly budget, challenging financial management. Therefore, if your loan has a variable interest rate, you should constantly monitor the ongoing interest rate trends and prepare for potential hikes in the EMIs.

Rising Personal Loan interest rates will impact borrowers differently based on whether they have fixed or floating-rate loans. While fixed interest rates offer protection and stability from repo rate hikes, variable rates are exposed to market fluctuations. Therefore, as a borrower, you must understand the loan terms and conditions completely and stay prepared for potential changes to avoid financial stress.

Impact of Increasing Interest Rates on New Personal Loans

Before applying for a Personal Loan, understanding the impact of rising interest rates on your loan plan is crucial. When the RBI increases the repo rate, loan companies must adjust their lending rates to cover the additional borrowing cost. Moreover, when Personal Loan interest rates rise, financial institutions become more cautious in approving the loan applications they receive. As a result, you will find it more challenging to obtain a loan at lower interest rates.

When applying for a Personal Loan, borrowers often encounter higher interest rates, leading to higher Equated Monthly Installments (EMIs) and increased overall loan costs. Consequently, the loan becomes more expensive, making repayment a greater challenge, especially if one’s income remains constant. This aligns with the fundamental objective of raising the repo rate: curbing inflation. When borrowing becomes more costly, fewer individuals opt for loans, resulting in decreased economic liquidity and subsequently contributing to the reduction of inflationary pressures.

Tips to Get Personal Loan Instant at Reasonable Interest Rates

To reduce the impact of increasing Personal Loan interest rates on new loan applications, you must consider comparing various loan terms and offers from different loan companies. Carefully review the loan terms before signing the loan agreement. Additionally, you can get a Personal Loan instant at a lower interest rate by following these tips:

- Improve Your Credit Score: A decent credit score will convince financial institutions of your credit behavior and repayment capacity. As a result, they may agree to approve your loan at a lower interest rate rather than risk their money with a high-risk borrower.

- Minimize Your DTI Ratio: If your DTI ratio is less than 30-40%, financial institutions feel assured of timely repayment without stressing your monthly budget. Pay off your outstanding debts, reduce monthly financial obligations, and find extra income sources to minimize your DTI ratio and get a Personal Loan instant at a lower interest rate.

- Provide Collateral: Applying for a loan and pledging an asset against it assured financial institutions of repayment even in a default. That is why interest rates for secured loans are lower than unsecured Personal Loans.

- Bring a Guarantor or Co-Applicant: Applying for a loan with a co-applicant or guarantor will provide double assurance to the financial institution of loan repayment. So, they may agree to offer you a loan at a lower interest rate.

What To Do When Personal Loan Interest Rates Rise?

If you plan to get an instant Personal Loan online, the most crucial step is to keep an eye on the current market trends and interest rates. RBI regularly revises the repo rate, eventually impacting the interest rate the financial institutions offer you. If the repo rate increases, your loan offer will also become costlier.

Since Personal Loans have fixed interest rates, wait for the rates to decline and apply at the right time. Once fixed, your rate will remain the same throughout the loan term. If it’s an emergency and you are forced to borrow a loan at a high-interest rate, you must still monitor the market trends and refinance the loan when the rates decrease. Borrowers with floating interest rate loans may also refinance their loans for a fixed-rate loan. Loan prepayments are also nice steps to reduce the impact of increasing interest rates, as they reduce the overall interest cost during the loan term.

Conclusion

As borrowers face the challenges of rising Personal Loan interest rates, it becomes increasingly vital to assess the financial implications and plan accordingly carefully. While the cost of borrowing may be on the upswing, borrowers can explore options like seeking competitive financial institutions and, when necessary, considering the possibility of getting a Personal Loan instantaneously to address their immediate financial needs. Being informed and proactive can empower borrowers to navigate these financial shifts more effectively and make informed decisions regarding their Personal Loans.

Related Topic –

Related Topic –

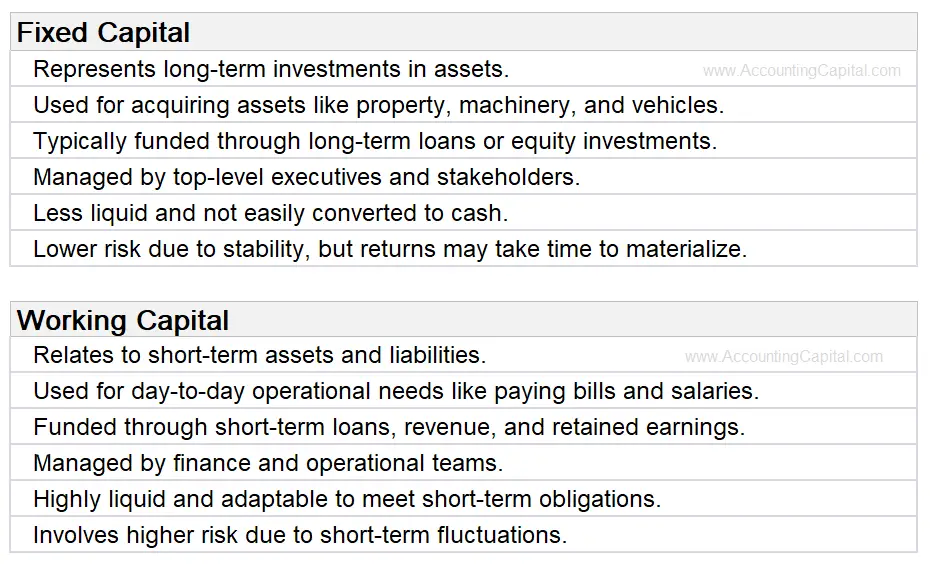

Both fixed and working capital are of equal importance for the existence and smooth functioning of the entity. Identifying the right source and amount of both fixed and working capital is a strategic task for an entity.

Both fixed and working capital are of equal importance for the existence and smooth functioning of the entity. Identifying the right source and amount of both fixed and working capital is a strategic task for an entity.